Atomico partner Tom Wehmeier reviews ‘The State of European Tech’ 2019 report

Atomico, the European venture capital firm founded by Skype’s Niklas Zennström, has released its latest annual The State of European Tech report, published in partnership with Slush and Orrick.

As part of the report, the authors surveyed 5,000 members of the ecosystem — including 1,000 founders — as well as pulling in robust data from other sources, such as Dealroom and the London Stock Exchange .

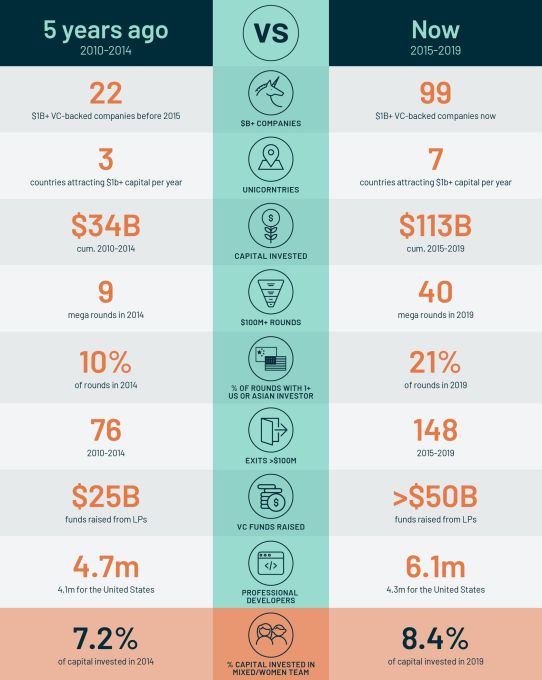

This year, the report reveals that the European tech ecosystem continues to mature and shows no sign of slowing — particularly highlighting the contrast from five years ago when the The State of European Tech report made its debut. Almost every key indicator is up and to the right, except, rather depressingly, diversity.

The data shows, for example, that competition for talent and access to the best founders has increased ferociously. And from a funding perspective, European founders have more choice than ever, especially with U.S. and Asian VC firms investing more and more in the region. Progress with gender diversity stalled, however, such as 92% of funding going to all-male teams.

I caught up with the report’s author Tom Wehmeier, Partner and Head of Insights at Atomico (also sometimes jokingly referred to as the “Mary Meeker of Europe”), where we discuss in more detail some of the key findings and why, it seems, that the rest of the world has finally woken up to Europe’s tech potential.

But first, a few headlines from the report:

- European technology companies are on track to raise a record 30$B+ in funding in 2019, up from $25B the year before. (Source: Dealroom)

- Despite failing to match the level of venture-backed exits of 2018, there was a record number of 40 $100M-plus deals as of September 2019, a size that many European tech sceptics did not believe was possible. (Source: Dealroom)

- A number of multi-billion-dollar non-venture backed companies like Nexi and Trainline made their debut on the public markets.

- European tech policymaking remains a mystery to many European founders.

- When asked to describe the top priority of the European Commission in terms of tech policy, 40% of founders and startup employees say they don’t feel informed enough to comment. (Source: survey)

- Despite this reported lack of awareness on policy issues, all respondents voted EU competition commissioner Margrethe Vestager as the person who had the most influence on European tech in 2019, good or bad. (Source: survey)

- European parliamentarians aren’t talking about fintech and digital health, two sectors which investors poured a combined $12.7bn into last year (Source: Politico and Dealroom)

- Europe’s diversity figures are still grim reading.

- In 2019, 92% of funding went to all-male teams, a similar level to 2018. (Source: Dealroom)

- There is still only one woman CTO in the 119 companies (<1%) based on a sample of executives in CxO positions at 251 European VC-backed tech companies that raised a Series A or B round between 1 October 2018 and 30 September 2019 with more than $10M funding, even though 7.5% of software engineers are women. (Source: Stack Overflow, Craft, Dealroom)

- Looking beyond gender diversity, ethnic minorities in tech experienced discrimination at a much high rate than white peers. (Source: survey)

- At least 80% of Black/African/Caribbean respondents who reported experiencing discrimination linked it to their ethnicity. (Source: survey)

- 63% of women VCs reported increased focus on attending events with stronger participation from diverse founders. The corresponding number for men VCs was only 33% of female respondents suggested that their male counterparts are leaving female VCs to fix Europe’s diversity problem. (Source: survey)

- European founders aren’t just aiming for commercial success — they are trying to solve some of the world’s largest problems.

- One in five European founders states that their company is already measuring its societal and/or environmental impact. (Source: survey)

- Only 14% of founders don’t believe it’s relevant for their company. Founders that are women are much more likely to be advanced in their approach to measuring impact. (Source: survey)

- Employees are placing a greater emphasis on corporate social responsibility, with 57% citing its importance in the State of European Tech survey. (Source: survey)

Extra Crunch: It is 5 years since Atomico published the first The State of European Tech report, which really attempted to capture a data-driven snapshot of the entire ecosystem. What are some of the biggest changes you’ve seen within European tech in the intertwining years or in this year in particular?

Tom Wehmeier: If I think back to when we did the first report, people who believe that Europe could actually be an interesting player in global technology, were largely limited to people who were in the tech industry in Europe itself. If you then fast forward to today, what has clearly happened — and I think 2019 was the year where this really materialized and became part of the narrative — was that belief translating from people on the inside to a bunch of people that were on the outside.

Most obviously has been the strength of interest from from the U.S. and the number of top-tier U.S. funds that are not just increasing their level of investment activity but committing to spending more and more time here on the ground, hiring people, building teams, building a network, and getting to know companies. I think it probably surprises people to know that 19% of all rounds this year will involve at least one U.S. investor in Europe, which is more than double since since the first year we did the report.

I think the other thing, where I come back to this idea that now we have finally convinced a certain group of people about the role that Europe can play, is mainstream institutional investors. I know it is not going to be lost on you, [but] this is going to be another record year for VC fund raising from Europe. And whilst the headline numbers might not be a surprise, I think what should catch people’s attention is that the composition of the LP base here in Europe is now shifting. And finally, there’s an unlocking of institutional investors, [by which] I mean pension funds, funds of funds, insurance companies, sovereign wealth funds, who are committing to European VC at levels that are significantly increased and elevated from where they had been in the past. So, if you just take pension funds, we’re going to see close to a billion dollars invested which is up nearly three fold.

It’s a validation of what’s happening around European tech to see that now coming through and I think is ultimately something that helps to build a foundation for the next five years of success. As much as this is a report that’s looking back, it’s also about trying to understand where things go from here.

With regards to the pension funds, do you think that is driven by the general bullishness towards European tech, or do you think it’s more the macro economic reality that maybe other places where they could put their money aren’t very attractive at the moment?

I think it’s really a reflection that there’s a strong level of belief that European venture as an asset class is an attractive investment opportunity. And that is reflected by the numbers. One of the charts that we’ve got in the report is from Cambridge Associates who do the benchmarking for the VC indices… And when you look back over a 1, 3, 5, or even a 10 year horizon, the performance from European VC is demonstrating that this is a place where for anyone building a diversified portfolio, they should have some allocation. I think it’s fundamentally the strength of the investment opportunity. That is the single biggest driver for why you’re seeing this happen.

I think the biggest thing that Europe has been able to prove is that it can take a great idea and turn it into a great company and that company can scale to not just a billion dollar outcome but to a multi-billion dollar outcome and go all the way through into an IPO or into a large scale acquisition. What you’ve seen happen in 2019 is in part A reflection of what happened last year where it was obviously this record year with Spotify, Adyen, Farfetch, Elastic and others that really showed you can go full cycle from start all the way to finish. And that the magnitude of those outcomes can be at a scale that makes them globally relevant.

Are the pension funds shifting their allocation of VC away from other geographies or are they just doing more VC as a whole?

Powered by WPeMatico