Asia

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to TechCrunch’s China roundup, a digest of recent events shaping the Chinese tech landscape and what they mean to people in the rest of the world.

The question for the tech news cycle in China these days has become: Who is Beijing’s next target? Regulatory clampdowns are common in China’s tech industry but the breadth of the recent moves has been unprecedented. No major tech giant is exempted and everyone is being attacked from a slightly different angle, but Beijing’s message is clear: Tech businesses are to align themselves with the interests and objectives of Beijing.

The government’s motivation isn’t always ideological. It could lead to policies that rein in the unruly private tutoring sector in the hope of easing pressure on students and parents. Recent orders from Beijing have strictly limited after-school tutoring, though they also sparked a wave of sympathy for public school teachers who work at lucrative tutoring centers to compensate for their meager salaries.

The effects of the education crackdown are also trickling down to internet companies. For the past few years, ByteDance had been aggressively building an online education business through a hiring and acquisition spree in part to diversify an ad-based video business. Its plan seems to be in shambles as it reportedly plans to lay off staff in its education department following recent the clampdown.

The restraints are also hitting American companies. Duolingo, the language learning app, was removed from several app stores in China. While it’s not immediately clear whether the action was the result of any policy change, the government recently, along with its restraints on extra-curriculum, barred foreign curricula in schools from K-9.

It could be tricky to read the top leaders’ minds because their messages could come through various government departments or state-affiliated media outlets, carrying different weights.

This week, Tencent is in the authorities’ crosshairs. About $60 billion of its market cap was wiped after the Economic Information Daily, an economic paper supervised by China’s major state news agency Xinhua, published an article (which was taken down shortly) describing video games as “spiritual opium” and cited the major role Tencent plays in the industry. Shares of Tencent’s smaller rival NetEase were also battered.

This certainly isn’t the first time Tencent and the gaming industry overall were slammed by the government for their impact on underage players. Tencent has been working to appease the authorities by introducing protections for young players, for instance, by tightening age checks several times.

Tencent, which has a sprawling online empire of social networks, payments and music on top of games, has also promised to “do [more social] good” through its products. And following the recent op-ed from the state paper, Tencent further restricted the amount of time and money children can spend inside games. But after all, the company still depends largely on addictive game mechanics that lure players to open loot boxes.

Tencent share prices over the past six months. Image Credits: Google Finance

The other camp of tech companies feeling the heat is those dependent on machine learning algorithms to distribute content. The Propaganda Department of the Chinese Communist Party, the country’s watchdog of public expressions, along with several other government organs, issued an advisory to “strengthen the study and guidance of online algorithms and carry out oversight over algorithmic recommendations.”

The government’s goal is to assert more control over how algorithmic black boxes affect what information people receive. Shares of Kuaishou, TikTok’s archrival in China, tanked on the news. Since its blockbuster initial public offering in February, Kuaishou’s stock price has tumbled as much as 70%. Meanwhile, the Beijing-based short video firm is shuttering one of its overseas apps called Zynn, which has caused controversy over plagiarism. But its overseas user base is also rapidly growing, crystalizing in one billion monthly users worldwide recently.

The week hasn’t ended. On Friday morning, The Wall Street Journal reported that the country’s antitrust regulator is preparing to fine Meituan, China’s major food delivery platform, $1 billion for allegedly abusing its market dominance. In 2020, Meituan earned 114.8 billion yuan or $17.7 billion in revenue.

Until recently, forcing suppliers to pick sides had been a common practice in China’s e-commerce world. Alibaba did so by forbidding sellers to list on rivaling platforms, a practice that resulted in a $2.75 billion antitrust penalty in April. We will see where the government will act next as it continues to curb the power of its tech darlings.

Powered by WPeMatico

Indian fintech startup BharatPe has raised $370 million in a new round of financing as it looks to aggressively scale its business in the next two years. It’s the nineteenth Indian startup to become a unicorn this year (up from 11 last year) as several high-profile global investors double down in the South Asian market.

The new round — a Series E — was led by Tiger Global and valued the New Delhi-based startup at $2.85 billion (post-money), it said in a statement Tuesday evening. Dragoneer Investor Group and Steadfast Capital also participated in the new round, which brings the startup’s to-date raise to over $580 million against equity.

Tuesday’s news confirms a TechCrunch scoop from June in which we reported that the four-year-old startup was looking to raise about $250 million at a pre-money valuation of $2.5 billion. BharatPe was valued at about $900 million in its Series D round in February this year, and $425 million last year.

BharatPe co-founder Ashneer Grover confirmed that the startup was indeed looking to raise $250 million until inbound requests from investors prompted an oversubscription. The new investment also includes some secondary transactions.

BharatPe, which counts Coatue, Ribbit Capital and Sequoia Capital India among its existing investors, operates an eponymous service to help offline merchants accept digital payments and secure working capital.

Even as India has already emerged as the second-largest internet market, with more than 650 million users, much of the country remains offline.

Among those outside of the reach of the internet are merchants running small businesses, such as roadside tea stalls and neighborhood stores. To make these merchants comfortable with accepting digital payments, BharatPe relies on QR codes and point of sale machines that support government-backed UPI payments infrastructure.

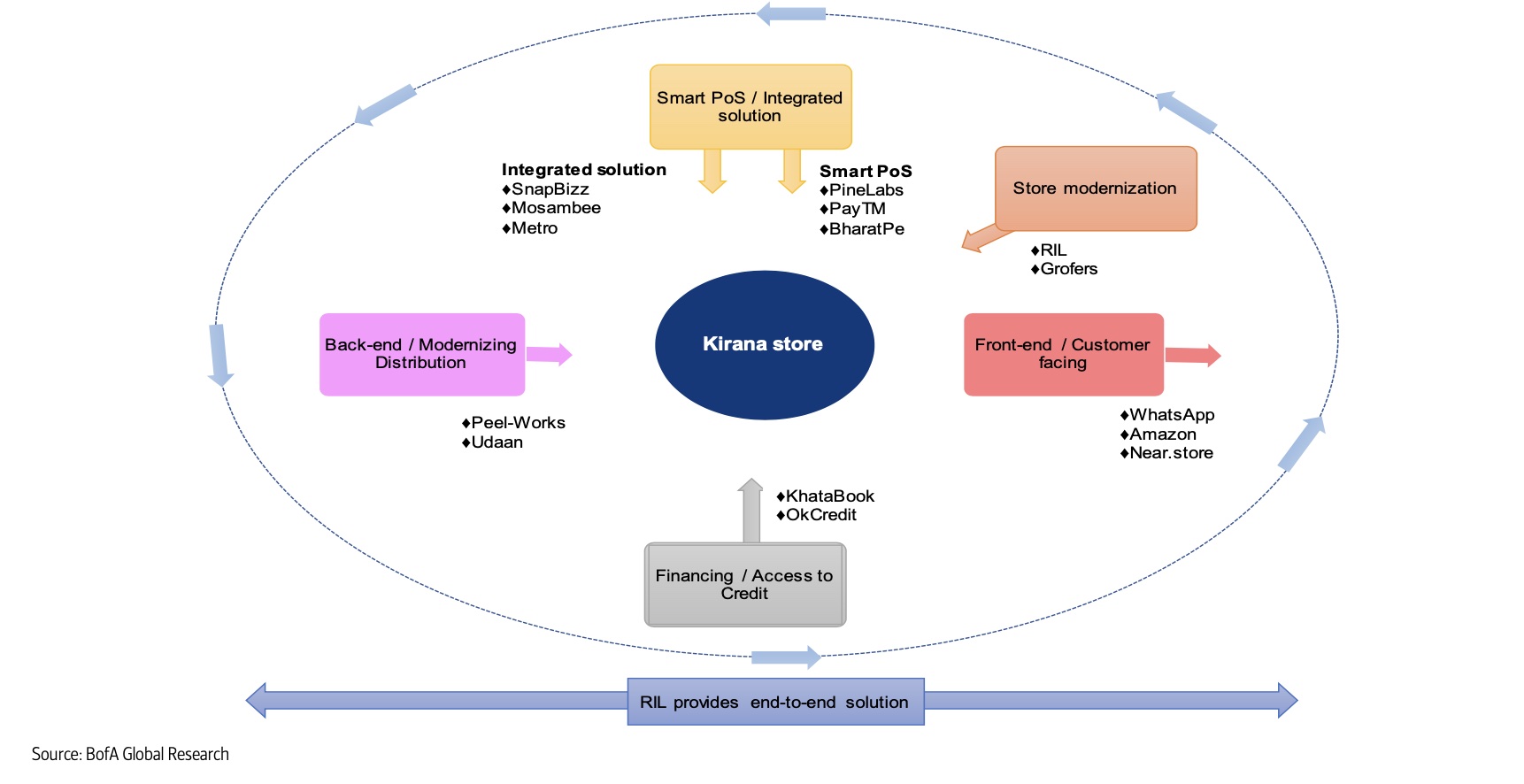

Scores of giants and startups are attempting to serve neighborhood stores in India. Image Credits: Bank of America Research

The startup, which serves more than 7 million merchants in over 130 Indian cities, said it has disbursed close to $300 million to merchant partners. It does not charge merchants for universal QR code access, but is looking to make money by lending.

The startup plans to expand its product offerings as well as work with Centrum Financial Services, with which it was recently granted the license by India’s central bank (Reserve Bank of India) to set up a small finance bank. (Centrum Financial Services has collaborated with BharatPe for the license, and the Indian startup says the two are “equal” partners.)

Tuesday’s development further illustrates the growing interest of Tiger Global in India. The New York-headquartered firm has backed dozens of Indian startups, including social commerce startup DealShare, edtech Classplus, Apna (an app that helps blue-collar workers connect with recruiters) and home services platform Urban Company in recent months.

On Tuesday, Infra.Market, an Indian startup that helps construction and real estate companies procure materials and handle logistics for their projects, said it had raised $125 million in a round led also by Tiger Global.

Powered by WPeMatico

Digital comics platform INKR’s team

INKR is a digital comics platform that crosses cultural and language divides, enabling creators to reach global audiences with its proprietary localization technology. Previously bootstrapped, the company announced today that it has raised $3.1 million in pre-Series A funding led by Monk’s Hill Ventures, with participation from manga distributor TokyoPop founder and chief executive Stu Levy and VI Management managing director David Do.

Headquartered in Singapore with an office in Ho Chi Minh City, INKR was founded in 2019 by Ken Luong, Khoa Nguyen and Hieu Tran. The company says that since it launched in October 2020, its monthly average users have grown 200%. It currently partners with more than 70 content creators and publishers, including FanFan, Image Comics, Kodansha USA, Kuaikan, Mr. Blue, SB Creative, TokyoPop and Toons Family, and has more than 800 titles so far, including manga, webtoons and graphic novels.

Luong, INKR’s CEO, told TechCrunch that the platform will focus first on translated comics from top global publishers, but plans to open to small and indie creators in 2022.

At the heart of INKR’s platform is its localization technology, which the company says reduces the time spent on preparing comics for different markets from days to just hours.

“Comics localization is more than just translation. It is a time-consuming process with many steps involving many people—file handling, transcription, translation, typesetting, sound effects, quality control, etc,” Luong said.

Some of the titles on INKR

In addition to language, publishers also have to take into account the differences between comic styles around the world, including Japanese manga, Chinese manhua, Korean manhwa, American comics. For example, comics can be laid out page-by-page or use vertical scrolling. Some languages read from left to right, while others go from right to left.

Luong says INKR’s proprietary AI engine, called INKR Comics Vision, is able to recognize different formats and elements on a comic page, including text, dialogue, characters, facial expressions, backgrounds and panels. INKR Localize, its tool for human translators, helps them deliver accurate translations more quickly by automating tasks like text transcription, vocabulary suggestions and typesetting.

Since localization is performed by teams, including people in different locations, INKR provides them with browser-based collaboration software. The platform supports Japanese-English, Korean-English and Chinese-English translations, with plans to add more languages. Some publishers, like Kuaikan Manhua and Mr. Blue, have used INKR to translate thousands of comic chapters from Chinese and Korean into English.

INKR provides content creators with a choice of monetization models, including ad-supported, subscription fees or pay-per-chapter. Luong says the platform analyzes content to tell publishers which model will maximize their earnings, and shares a percentage of the revenue generated.

INKR is vying for attention with other digital comics platforms like Amazon-owned Comixology and Webtoon, the publishing portal operated by Naver Corporation.

Luong said INKR’s competitive advantages include the the diversity of comics is offers and the affordability of its pricing. Before launching, it also invested in data and AI-based technology for both readers and publishers. For example, users get personalized recommendation based on their reading activity, while publishers can access analytics to track title performance based on consumption trends.

In a statement, Monk’s Hill Ventures general partner Justin Nguyen said INKR’s “proprietary AI-driven platform is addressing pain points for creators and publishers who need to go digital and global—localizing for many languages quickly and cost-effectively while also helping them improve reach and readership through analytics and intelligent personalized feeds. We look forward to partnering with them to quench the huge demand for translated comics globally.”

Powered by WPeMatico

Business-to-business payments platform Nium announced Monday that it raised more than $200 million in Series D funding and saw its valuation rise above $1 billion.

The company, now Singapore-based but shifting to the Bay Area, touted the investment as making it “the first B2B payments unicorn from Southeast Asia.”

Riverwood Capital led the round, in which Temasek, Visa, Vertex Ventures, Atinum Capital, Beacon Venture Capital and Rocket Capital Investment participated, along with a group of angel investors like DoorDash’s Gokul Rajaram, FIS’ Vicky Bindra and Tribe Capital’s Arjun Sethi. Including the new funding, Nium has raised $300 million to date, Prajit Nanu, co-founder and CEO, told TechCrunch.

The B2B payments sector is already hot, yet underpenetrated, according to some experts. To give an idea just how hot, Nium was seeking $150 million for its Series D round, received commitments of $300 million from eager investors and settled on $200 million, Nanu said.

“This is our fourth or fifth fundraise, but we have never had this kind of interest before — we even had our term sheets in five days,” he added. “I believe this interest is because we’ve successfully managed to create a global platform that is heavily regulated, which gives us access to a lot of networks. This is an environment where payment is visible, and our core is powering frictionless commerce and enabling anyone to use our platform.”

Nium’s new round adds fuel to a fire shared by a number of companies all going after a global B2B payments market valued at $120 trillion annually: last week, Paystand raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments. In March, Higo brought in $3.3 million to do the same in Latin America, while Balance, developing a B2B payments platform that allows merchants to offer a variety of payment methods. raised $5.5 million in February.

Nium’s approach is to provide access to a global payment infrastructure, including card issuance, accounts receivable and payable, and banking-as-a-service through a single API. The company’s network enables customers to then send funds to more than 100 countries, pay out in more than 60 currencies, accept funds in seven currencies and issue cards in more than 40 countries, Nanu said. The company also boasts money transfer, card issuances and banking licenses in 11 jurisdictions.

Francisco Alvarez-Demalde, co-founding partner and managing partner at Riverwood, said in an email that the combination of software — plus regulatory licenses — and operating a fintech infrastructure platform on behalf of neobanks and corporates is a global trend experiencing hyper-growth.

Riverwood followed Nium for many years, and its future vision was what got the firm interested in being a part of this round. Alvarez-Demalde said that “Nium has the incredible combination of a great market opportunity, a talented founder and team, and we believe the company is poised for global growth based on underlying secular technology trends like increasing real-time payment capabilities and the proliferation of cross border commerce.

“As a central payment infrastructure in one API, Nium is a catalyst that unlocks cross-border payments, local accounts and card issuance with a network of local market licenses, partners and banking relationships to facilitate moving money across the world,” he added. “Enterprises of all types are embedding financial services as part of their consumer experience, and Nium is a key global enabler of this trend.”

Nanu said the new funding enables the company to move to the United States, which represents 3% of Nium’s revenue. He wants to increase that to 20% over the next 18 months, as well as expand in Latin America. The investment also gives the company a 12- to 18-month runway for further M&A activity. In June, Nium acquired virtual card issuance company Ixaris, and in July acquired Wirecard Forex India to expose it to India’s market. He also plans to expand the company’s payments network infrastructure, invest in product development and add to Nium’s 700-person headcount.

Nium already counts hundreds of enterprise companies as clients and plans to onboard thousands more in the next year. The company processes $8 billion in payments annually and has issued more than 30 million virtual cards since 2015. Meanwhile, revenue grew by over 280% year over year.

All of this growth puts the company on a trajectory for an initial public offering, Nanu said. He has already spoken to people who will help the company formally kick off that journey in the first quarter of 2022.

“Unlike other companies that raise money for new products, we aim to expand in the existing sets of what we do,” Nanu said. “The U.S. is a new market, but we have a good brand and will use the new round to provide a better experience to the customer.”

Powered by WPeMatico

China’s e-commerce and industrial ecosystem is as different from the Western world as its culture. The country took decades to earn its reputation as the Factory of the World, but it now boasts a supply chain and manufacturing ability that few countries can match.

Creative use of the country’s networked manufacturing and logistics hubs make mass production both cheap and easy. Clothing, electronics, toys, automobiles, musical instruments, furniture — you name it and you’ll find a manufacturer in China who can turn your intangible concept into mass-manufacturable reality in mere days. And they’ll do it for cheaper than anywhere else in the world.

It was just a matter of time until an intrepid Chinese entrepreneur with a tech background decided to take on Coca-Cola and PepsiCo.

China is also home to one of the world’s largest e-commerce and tech ecosystems. Hundreds of startups dot the landscape, and the amount of money being raised and spent on innovating around the country’s industrial heft is mind-boggling.

So it was just a matter of time until an intrepid Chinese entrepreneur with a tech background decided to take on Coca-Cola and PepsiCo. The tech revolution hasn’t yet affected the bottled beverage industry quite as much as it has others. Incumbent giants therefore could lose a sizable chunk of market share if a company could just manage to weave together China’s manufacturing proficiency and agility with the modern tech startup philosophy of “moving fast and breaking stuff.”

Genki Forest, a Chinese direct-to-consumer (D2C) bottled beverage startup, is one such contender. A philosophy centered around iteration informed by data, quick turnarounds and a laser focus on taking advantage of China’s huge e-commerce ecosystem has helped this company’s revenues rise rapidly since it started five years ago. Its sugar-free sodas, milk teas and energy drinks sell in 40 countries and generated revenue of about $450 million in 2020. The company aims to reach $1.2 billion this year.

If anything, Genki Forest’s valuation has shot up even faster. It recently completed its fourth VC round that values it at a whopping $6 billion, triple the price it fetched a year earlier, and it has so far raised at least half a billion dollars.

It’s striking how closely Genki Forest’s operations resemble that of a tech startup. So we thought we should take a closer look and see what this company’s graph can tell us about the new wave of Chinese D2C entrepreneurship looking to take over the globe.

The bottled beverage industry wasn’t what Genki Forest’s founder, Binsen Tang, initially set out to tackle. His first startup was a successful casual, mostly mobile gaming outfit known as ELEX Technology. It was nowhere near record-breaking, though — some 50 million users logged on to a few popular games in over 40 countries worldwide, including one of the first versions of Happy Farm, a predecessor to Zynga’s Farmville. But Tang wasn’t satisfied and eventually sold ELEX Technology to a publicly listed company for about $400 million in 2014.

Tang would walk away with a few important lessons. He’d learned by now that Chinese products were already competitive globally, whether people realized it or not, and that and geographic arbitrage was real, Happy Farm being the perfect example of this. Lastly, he now knew that it was far more important to choose the right “racetrack” (as Chinese investors and entrepreneurs like to put it) than to have a great product.

Picking the right race to win was perhaps the most important takeaway. It’s also an idea that sets Chinese entrepreneurs apart from their Western counterparts — the most worthwhile endeavors are in identifying the largest and most rewarding market at hand, regardless of one’s previous expertise. It was what led Zhang Yiming to create ByteDance, and Lei Jun to found Xiaomi.

That very philosophy led Tang to build Genki Forest. After selling ELEX Technology, Tang didn’t go back to the business that netted him his first pot of gold. As much as he had benefited from the rise of the mobile internet, he thought there was a far bigger opportunity building a consumer brand and applying the lessons he learned from programming to the manufacture of tangible products.

He soon set up his own investment fund, Challenjers Capital, convinced that the next big tech opportunity in China was in tech’s application to everyday consumer products. He soon began to invest in everything from ramen and hotpots to bottled beverages.

China’s quickly expanding e-commerce ecosystem and the plethora of D2C businesses flourishing on Alibaba and JD.com would also influence his decision to sell directly to his target audience rather than take the traditional route. But to truly understand his motivations, we need to take a look at the extremely unique D2C environment in China and how it has changed over the years.

“China doesn’t need any more good platforms,” Tang told his team in an internal email in 2015, “but it does need good products.” Tang was talking about how the age of building infrastructure for e-commerce in China was largely over; it was now time to create brands that could take advantage of the advanced distribution network that had been laid out.

Other investors noticed as well. Albus Yu, principal at China Growth Capital, told me that his fund had stopped making investments in independent consumer-facing platforms or marketplaces for a while. “2014 might have been the last year it was economically feasible to start such a business due to the soaring cost of acquiring customers and the strength of incumbents,” he said.

Indeed, 2015 was the year when CACs began to exceed or at least rival ARPUs for Alibaba and JD.com.

In China, that distribution network was present across the digital and physical worlds. Online, there was immense market power concentrated in the hands of just two players: Alibaba and JD.com, which used to have, and still maintain, 80% or above in market share.

In fact, the dominance of Alibaba, in particular, was so overwhelming that for years, VCs invested not in D2C, but in “Taobao brands,” since that was the only channel one needed to conquer in order to make it.

Customer acquisition was therefore straightforward — throw everything into advertising on Alibaba’s Tmall platform, especially during its annual flagship shopping festival, Singles’ Day. Even today, garnering a top spot in one of the category leaderboards remains a surefire way to build brand awareness, investor interest, as well as sales records.

Physically, the Chinese market also differs greatly from much of the developed West. Years of heavy investment in logistics by the private sector, accelerated by government support and infrastructure buildout, means that delivery costs have come down significantly over the years, even dipping below $0.40 per package wholesale as of this year. Innovations such as return insurance have also sped up customer adoption.

By 2016, China was shipping 30 billion packages a year, already accounting for 44% of global shipments. That number has been doubling every three years and is expected to exceed 100 billion this year. And the low cost of delivery is one of the biggest reasons for China’s outsized e-commerce market — the largest globally and estimated to reach $2.8 trillion in 2021, more than triple that of the No. 2, the U.S.

Express parcels sit stacked at a logistic base of e-commerce giant Suning before the 618 Shopping Festival. Image Credits: VCG

Present-day China also presents another edge: Proximity to an advanced, flexible manufacturing network and supply chain for the vast majority of consumer products, and the ability to outsource almost everything to them.

The original equipment manufacturers of years past have long since evolved into original design manufacturers. An expected consequence of being “the Factory of the World” for so many years, making goods for some of the best brands in the world, is that some of the knowledge was bound to transfer.

It may be difficult for outsiders to understand just how strong China’s networked manufacturing hubs are these days. What used to take weeks now takes mere days, the lead times shortened drastically by software, robots and other advancements. For example, Chinese cross-border ultra-fast-fashion company Shein has compressed design-to-ship timelines to as little as seven days.

And it’s definitely not just for making crop tops. The turnaround can be astonishingly fast even when manufacturing completely unfamiliar goods, such as when electric vehicle maker BYD turned its factory into the world’s largest face mask plant in just two weeks when the COVID-19 pandemic struck last year.

Companies leverage this manufacturing flexibility and agility for more than just speed. Chinese cosmetics upstart Perfect Diary uses it to launch twice as many SKUs as foreign competitors. In addition, the quick turnaround allows agile brands to take advantage of that most ephemeral of IP, memes.

It’s not to say that the Chinese supply chain is inaccessible to foreign entrepreneurs. Best-selling mattress maker Zinus, for example, is founded by a South Korean, but its products are manufactured in China and sold mostly on Amazon to U.S. customers.

It’s just that very few non-Chinese companies have figured out how to tap as deeply into the supply chain as this new crop of Chinese D2C brands, which can require years of working not just alongside but physically inside the factories, building trust and know-how. Shein, for example, watches carefully what other brands are making by staying close to the factories.

Before global sensations such as TikTok weakened the mantra, “copy to China” used to be a dominant characterization of Chinese startups. In December 2015, when Tang registered the Genki Forest trademark, that was still very much a relevant strategy.

Powered by WPeMatico

News that China’s government may force domestic tutoring-focused companies to go nonprofit is taking a huge bite out of the value of several technology companies. Bloomberg notes that the value of companies like New Oriental Education & Technology Group and TAL Education are tumbling in light of the news, which would constitute merely the latest salvo against tech companies in the autocratic country.

New Oriental’s Hong Kong-listed shares fell 44.22% in after-hours trading after the nonprofit news broke, while NYSE-shares of TAL are off an even sharper 51.75% in pre-market trading. With Yahoo Finance listing a roughly $13.8 billion market cap for TAL ahead of its impending declines at the market open, billions of equity value are about to get deleted. The list goes on: China Online Education Group is off 39.97% in after-hours trading, for example.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

A new decision by China’s government to exert more control over a sector of its domestic economy should not surprise. And we shouldn’t be shocked that online tutoring is in the country’s targets; today’s news is a follow-up to prior regulatory action in the sector from earlier in the year.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

For example, what will happen to Yuanfudao? The company was valued at $15.5 billion last year, offering what TechCrunch described as “live tutoring, an online Q&A arm and a math-problem-checking arm.” Will the company see its wings clipped?

Or how about Zuoyebang, which raised $1.6 billion in a single round last year? TechCrunch wrote that Zuoyebang offers “online courses, live lessons and homework help for kindergarten to 12th grade students.” Is it in trouble as well?

All this comes on the same day that shares in Zomato began to float, with the Indian online food delivery company seeing its shares close up nearly 65% in their first day’s trading. TechCrunch has viewed the Zomato IPO as a possible bellwether for the larger Indian startup market, and the results augur well for other growth-focused, loss-making unicorns in the country.

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Syfe founder Dhruv Arora

Investment apps in Southeast Asia are attracting a lot of funding, and now some are raising fast follow-on rounds, too. For example, Indonesian robo-advisor app Bibit raised $65 million in May just four months after a $30 million growth round. Now Singapore-based Syfe is announcing that it has closed a $40 million SGD (about $29.6M USD) Series B, only nine months after its Series A. It also said all of Syfe’s full-time employees will receive equity in the company.

The latest round’s lead investor is Valar Ventures, which also led Syfe’s Series A, marking the fintech-focused venture capital firm’s first investment in an Asian startup. Returning investors Presight Capital and Unbound participated, too.

This brings Syfe’s total raised so far to $70.7 million SGD (about $52.3 million USD) since it was founded in 2019. The startup did not disclose its Series B post-money valuation, but founder and chief executive officer Dhruv Arora told TechCrunch it increased 3.6 times from its Series A. The company also hasn’t disclosed total user numbers, but assets under management have grown four times since January, thanks in large part to user referrals and the launch of new products like Syfe Cash+ and Core portfolios.

“To be honest, we weren’t really looking to raise a Series B,” Arora told TechCrunch. “We saw some of the positive outcomes of resources from our Series A. We really scaled up the team and started launching new products and options for our users.” Syfe probably could have waited another six months to a year to raise a new round, he added, but its investors approached the startup again and offered good terms for another round.

About 50% to 70% of new users each month come through recommendations from existing customers, which keeps Syfe’s acquisition costs extremely low, Arora says. Since the beginning of this year, it has also doubled its team in Singapore to more than 100 people, allowing the startup to explore different kind of distribution strategies and partnerships. The app currently has users in 42 countries, but only actively markets in Singapore, where it holds a Capital Markets Services license from the Monetary Authority of Singapore (MAS). It has plans to announce a second market soon.

Syfe was founded in 2017 and launched its app in July 2019. Prior to starting Syfe, Arora was an investment banker at UBS Investment Bank before serving as vice president and head of growth at Indian grocery delivery startup Grofers.

While retail investment rates are still low in Southeast Asia, interest has jumped significantly over the past year. One of the reasons most commonly cited is the economic impact of COVID-19, which motivated people to earn returns from their money instead of keeping it in saving accounts.

“Most of my career has been within Hong Kong, Singapore and parts of India. I think culturally we’ve always been told to save, save, save,” Arora says. “It made sense because banks were giving good interest rates, but now the majority of economies are in negative real rate of interest.” Along with consumers’ growing familiarity with online wallets and other digital financial services, this set the stage for investment apps to come in, attracting customers who might not have gone to traditional brokerages.

Arora says he expected people to become more interested in investing, but gradually, over the course of about five to seven years. Instead, that shift is happening much more quickly. “My view is that tomorrow’s saving accounts become smart investing accounts. That’s been my view ever since we started Syfe, but this last year has made it evident that it has to happen and has to happen much bigger. So I think this wave will continue,” he says.

While many investment apps focus on millennial users, Syfe’s target demographic is wider. In the last six to nine months, Arora says there has been an uptick in users aged 50 and above on the platform, and its oldest user is 93 years old.

“The users in that segment have become a bigger percentage and the reality is that they typically have more disposable income. The average customer in their 50s will deploy, in our experience, almost twice the more conventional demographic which might be between 30 to 40,” says Arora.

Out of the many investment apps that have emerged in Southeast Asia, users most often compare Syfe to Stashaway, Endowus and Autowealth when shopping around for a platform. Arora says the space has a lot of room to grow because retail investment in the region is still very low. “I think it’s still super early in the game. There is enough room for multiple players and I think more will come into this domain, because if you can get your acquisition metrics into place, this can be a very profitable business.”

In terms of differentiating, Syfe is focused on new product development and user localization and personalization so customers can create more customized portfolios.

Syfe has a team of financial advisors for users who want person-to-person consultations, but Arora says most of Syfe’s investors rely entirely on its app to decide how to invest. Over the last nine months, it has only added one new advisor to its team, while focusing on making its user interface more intuitive.

“The human touch is optional, but it’s not necessary and in many cases, it’s only needed to help people understand the offering once,” says Arora. “But our goal is always going to be technology company and for the app to become so intuitive that whether you are 18 or 93, you are able to use the offering with very limited guidance.”

In a press statement, Valar Ventures founding partner Andrew McCormack says, “Syfe was our first investment in Asia and we’ve been impressed by its rapid, sustained growth over the past couple of years. The opportunity for the company to meet the saving and investment needs of a burgeoning mass-affluent consumer population in Asia remains significant, and we are confident that Syfe will continue to expand at pace.”

Powered by WPeMatico

Shares of Chinese ride-hailing business Didi are off 22% this morning after the company was hit by more regulatory activity over the holiday weekend. The recently public company traded as high as $18.01 per share since it held an IPO last week; today, shares of Didi are worth just $12.09, off around a third from their 52-week high.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The decline in value follows a review by a Chinese cybersecurity agency that led to Didi being unable to onboard new users, a decision that arrived as last week rolled to a close.

Over the weekend, Didi was hit with more regulatory action. This time, the Cyberspace Administration of China said, via an internet translation, that “after testing and verification, the ‘Didi Travel’ App [was found to have] serious violations of laws and regulations in collecting and using personal information,” which led the agency to command app stores “to remove the ‘Didi Travel’ app, and required [the company] to strictly follow the legal requirements and refer to relevant national standards to seriously rectify existing problems.”

Over the weekend, Didi was hit with more regulatory action. This time, the Cyberspace Administration of China said, via an internet translation, that “after testing and verification, the ‘Didi Travel’ App [was found to have] serious violations of laws and regulations in collecting and using personal information,” which led the agency to command app stores “to remove the ‘Didi Travel’ app, and required [the company] to strictly follow the legal requirements and refer to relevant national standards to seriously rectify existing problems.”

Being yanked from relevant app stores was enough for Didi to alert investors that its mobile app “had the problem of collecting personal information in violation of relevant PRC laws and regulations.” Didi said that the change in its app availability “may have an adverse impact on its revenue in China.”

Understatement of the year, I reckon.

But there’s more going on than what Didi is enduring. As CNBC reported:

Powered by WPeMatico

Influential entrepreneurs like Paul Graham and Naval Ravikant always preach the need for startups to have founders-turned-investors on their cap table. As Ravikant puts it, “founders want to know that the people they are taking money from have first-hand experience.”

His platform AngelList has helped individual founders-cum-investors source and participate in deals via collectives. However, some venture firms have taken this up a notch by bringing founders to create a fund and invest together.

Today, one of such, MAGIC Fund, a global collective of founders, is announcing that it has raised a second fund of $30 million to continue backing early-stage startups across Africa, Europe, Latin America, North America, and Southeast Asia.

Since the firm’s first fund launched in 2017, MAGIC has invested in 70 companies at pre-seed and seed stages across these emerging markets. Some of these companies include Retool, Novo, Payfazz, and Mono.

MAGIC Fund has 12 founders who act as general partners. TechCrunch caught up with managing partner Adegoke Olubusi and operating partner Matt Greenleaf to learn more about the fund’s thesis and activities.

Olubusi, who had built and exited a couple of startups over the years, also dabbled with angel investing for some time. In 2017, Olubusi’s current startup Helium Health got accepted into Y Combinator. It was there he met more founders like him who were angel investors with impressive portfolios. The interesting bit? Each founder wanted to invest in other companies during YC’s Demo Day.

“So about three years ago, I was at YC, and I was going to invest in my own batch. I was pitching on the day, but I was also listening to other pitches. However, it wasn’t just me; there were many other founders as well,” Olubusi said.

After building and exiting multiple startups, some founders turn into angel investing to support startups and their ecosystems. However, most of them tend to go alone and are stuck with cutting checks in their local markets, which limits opportunities.

Some MAGIC portfolio companies

Here’s a scenario. In 2016, when unicorns Flutterwave and Kavak raised their seed rounds in Nigeria and Mexico respectively, an African biotech founder who knew about Kavak and a Latin American edtech founder interested in African fintech would not have had the capacity to evaluate those deals even if they wanted; the reason being a lack of reach and experience in both the industry or geography.

Olubusi and the other founders knew this would be a limitation in the long run if they went solo. Thus, they decided to create MAGIC. The idea was to bring global founders together with diverse skillsets in diverse industries and geographies to evaluate deals better and drive value for each other. Hence, they can participate in two unicorns instead of one.

“Instead of us investing individually because obviously, we have somewhat limited capacity in terms of how much time we have as founders because of our respective companies, why don’t we collaborate on a strategy together and co-invest together?”

“The way we thought of MAGIC was a fund of micro funds built by founders for founders,” Greenleaf continued.

In some of the personal conversations I’ve had with founders about their investors, a recurring theme has been that the most useful investors didn’t necessarily sign the biggest checks. It’s a theme Olubusi also relates to all too well.

“It was like every time we think about it, everyone who gave the most money rarely had time for us. It was so frequent that we all identified this as an actual thing. What actually drove value for us were other investors who were founders and operators, and other experienced people who were able to help us find product-market fit and fight regulators. These were actually the people in the trenches with us.”

Olubusi believes the early-stage part of investing, particularly in pre-seed and seed, is where VCs who are founder-operators find their sweet spot. They are precious when startups are trying to figure out product-market fit. And unlike traditional investors who are looking to get multiples on investments, Olubusi argues that for founders-investors, what matters is how much value they can drive for startups.

Image Credits: MAGIC Fund

MAGIC’s play is even more essential considering that it also plays in emerging markets where on-the-ground operational help is needed in industries with numerous unknowns and uncertainties.

“There is so much money in the market now and early-stage decision making at pre-seed and seed should be left in the hands of founders. Because think about it really, to make an evaluation of whether I should invest in a healthcare or fintech company in Africa, it makes sense to have those who’ve spent years battling through it in the trenches make those decisions. And what we’re trying to do with the fund is publish as much information as possible and keep performing at the 100 percentile and say this is still the best strategy and is very scalable.”

MAGIC Fund 1 was $1.5 million and Olubusi says the investments performed 5x over the period of three years. As some of these companies exited, their founders invested in MAGIC and came on board as Fund 2 partners.

MAGIC has also enlisted additional investors who, according to Olubusi, are respected for their investing abilities and ecosystem support. For instance, Olugbenga Agboola, Flutterwave CEO, is known across the African tech ecosystem as a founder who goes out of his way to help established and up-and-coming fintech companies. Hendra Kwik of Payfazz has such a reputation in Southeast Asia as well. They, alongside other founders, join MAGIC as limited partners.

Per the firm’s statement, one-third of the entire fund was contributed by the founder GPs. For its LPs, diversity play is considered as 50% of them are black while 33% are women. Some of them include Michael Seibel, Tim Draper, Rappi’s Andres Bilbao, Paystack’s Shola Akinlade, Katie Lewis, and Octopus Ventures’ Kirsten Connell. For its partners, MAGIC has brought on the likes of Stitchroom’s Tom Chen, Medumo’s Adeel Yang, Juice’s Michael Lisovetsky, and Troy Osinoff, and Evercare’s Temi Awogboro.

Magic Fund 2 will be writing $100,000 to 300,000 checks at pre-seed and seed stages focusing on fintech, healthcare, SaaS and enterprise, women’s health, developer tools.

What does the fund look for in founders? Olubusi gives two answers. One, MAGIC wants to back founders with incentives to stick through the hard times of a company.

“At pre-seed and seed, you don’t have enough data about a company to make an investment decision. Your bet is entirely on the founder and the founding team. What we know, having done this several times, is that things get harder. So when we’re looking at the founder, we’re evaluating whether or not the founder has the grit to stick through the toughest times which are going to come up.”

The second indicator factors if the founder has the willingness, openness, the flexibility to learn and use that knowledge to succeed. Greenleaf believes these strategies have incredibly helped the firm fund exceptional companies and maintain good relationships with founders.

“Most of these founders don’t view us as their investors. They view us as fellow founders who are helping them along their journey. I think that also ties into them keeping it real with us and allows us to see them as people, and not just founders. That’s one of the things that have worked in our favor,” he said.

Powered by WPeMatico