First Round Capital

Auto Added by WPeMatico

Auto Added by WPeMatico

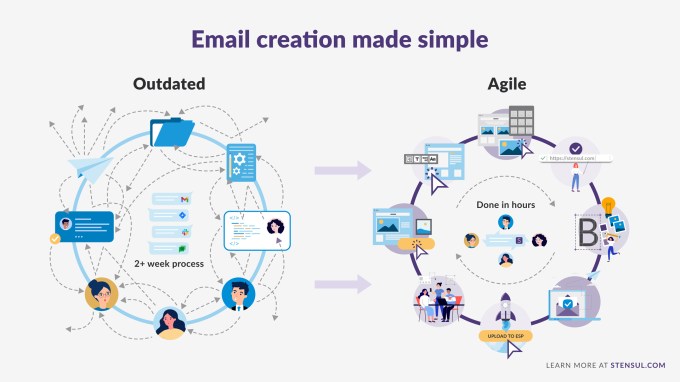

Stensul, a startup aiming to streamline the process of building marketing emails, has raised $16 million in Series B funding.

When the company raised its $7 million Series A two years ago, founder and CEO Noah Dinkin told me about how it spun out of his previous startup, FanBridge. And while there are many products focused on email delivery, he said Stensul is focused on the email creation process.

Dinkin made many similar points when we discussed the Series B last week. He said that for many teams, creating a marketing email can take weeks. With Stensul, that process can be reduced to just two hours, with marketers able to create the email on their own, without asking developers for help. Things like brand guidelines are already built in, and it’s easy to get feedback and approval from executives and other teams.

Dinkin also noted that while the big marketing clouds all include “some kind of email builder, it’s not their center of gravity.”

He added, “What we tell folks [is that] literally over half the company is engineers, and they are only working on email creation.”

Image Credits: Stensul

The team has recently grown to more than 100 employees, with new customers like Capital One, ASICS Digital, Greenhouse, Samsung, AppDynamics, Kroger and Clover Health. New features include an integration with work management platform Workfront.

Plus, with other marketing channels paused or diminished during the pandemic, Dinkin said that email has only become more important, with the old, time-intensive process becoming more and more of a burden.

“We need more emails — whether that’s more versions or more segments or more languages, the requests are through the roof,” he said. “The teams are the same size … and so that’s where especially the leaders of these organizations have looked inward a lot more. The ways that they have been doing it for years or decades just doesn’t work anymore and prevents them from being competitive in the marketplace.”

The new round was led by USVP, with participation from Capital One Ventures, Peak State Ventures, plus existing investors Javelin Venture Partners, Uncork Capital, First Round Capital and Lowercase Capital . Individual investors include Okta co-founder and COO Frederic Kerrest, Okta CMO Ryan Carlson, former Marketo/Adobe executive Aaron Bird, Avid Larizadeh Duggan, Gary Swart and Talend CMO Lauren Vaccarello.

Dinkin said the money will allow Stensul to expand its marketing, product, engineering and sales teams.

“We originally thought: Everybody who sends email should have an email creation platform,” he said. “And ‘everyone who sends email’ is synonymous with ‘every company in the world.’ We’ve just seen that accelerate in that last few years.”

Powered by WPeMatico

The global legal services industry was worth $849 billion in 2017 and is expected to become a trillion-dollar industry by the end of next year. Little wonder that Steno, an LA-based startup, wants a piece.

Like most legal services outfits, what it offers are ways for law practices to run more smoothly, including in a world where fewer people are meeting in conference rooms and courthouses and operating instead from disparate locations.

Steno first launched with an offering that centers on court reporting. It lines up court reporters, as well as pays them, removing both potential headaches from lawyers’ to-do lists.

More recently, the startup has added offerings like a remote deposition videoconferencing platform that it insists is not only secure but can manage exhibit handling and other details in ways meant to meet specific legal needs.

It also, very notably, has a lending product that enables lawyers to take depositions without paying until a case is resolved, which can take a year or two. The idea is to free attorneys’ financial resources — including so they can take on other clients — until there’s a payout. Of course, the product is also a potentially lucrative one for Steno, as are most lending products.

We talked earlier this week with the company, which just closed on a $3.5 million seed round led by First Round Capital (it has now raised $5 million altogether).

Unsurprisingly, one of its founders is a lawyer named Dylan Ruga who works as a trial attorney at an LA-based law group and knows first-hand the biggest pain points for his peers.

More surprising is his co-founder, Gregory Hong, who previously co-founded the restaurant reservation platform Reserve, which was acquired by Resy, which was acquired by American Express. How did Hong make the leap from one industry to a seemingly very different one?

Hong says he might not have gravitated to the idea if not for Ruga, who was Resy’s trademark attorney and who happened to send Hong the pitch behind Steno to get Hong’s advice. He looked it over as a favor, then he asked to get involved. “I just thought, ‘This is a unique and interesting opportunity,’ and said, ‘Dylan, let me run this.’ ”

Today the 19-month-old startup has 20 full-time employees and another 10 part-time staffers. One major accelerant to the business has been the pandemic, suggests Hong. Turns out tech-enabled legal support services become even more attractive when lawyers and everyone else in the ecosystem is socially distancing.

Hong suggests that Steno’s idea to marry its services with financing is gaining adherents, too, including amid law groups like JML Law and Simon Law Group, both of which focus largely on personal injury cases.

Indeed, Steno charges — and provides financing — on a per-transaction basis right now, even while its revenue is “somewhat recurring,” in that its customers constantly have court cases.

Still, a subscription product is being considered, says Hong. So are other uses for its videoconferencing platform. In the meantime, says Hong, Steno’s tech is “built very well” for legal services, and that’s where it plans to remain focused.

Powered by WPeMatico

As a founding member of TI Platform Management, I have quarterbacked more than $200 million in investments into first-time fund managers around the world. That portfolio includes being one of the first institutional checks into Atomic Labs ($170+ million, SaaStr ($160+ million) and Entrepreneur First ($140+ million), among many others.

Having seen successful returns as a fund manager and an early-stage VC (as well as recently raising my own angel fund), I’ve formulated several best practices and strategies for investing in fund managers. If you want to raise your first fund, here’s how.

Just as VCs bucket startup founders into categories, limited partners (the investors in your venture fund, also known as “LPs”) have an unwritten way of categorizing venture managers. The vast majority fit one of three archetypes:

Here’s how each is perceived by institutional LPs and the unique blockers they have to overcome:

Having been through the journey of starting a company, former founders/operators often have strong intuition in identifying founders and an empathy/rapport that raises their win-rate on deals. Additionally, having built an innovative company, they can bring special insights in where the market is headed. Building a company, however, requires different skills from founding a fund.

If you’re a former founder/operator turned VC, expect LPs to ask questions that suss out:

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Airbnb’s issues. Before that, I noted Uber’s new “money” team.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you’re new, you can subscribe to Startups Weekly here.

Three African fintech startups; OPay, PalmPay and East African trucking logistics company Lori Systems, closed large fundraises this year. On their own, the deals aren’t particularly notable, but together, they expose a new trend within the African startup ecosystem.

This year, those three companies brought in a total of $240 million in venture capital funding from 15 different Chinese investors, who’ve become increasingly active in Africa’s tech scene. TechCrunch reporter Jake Bright, who covers African tech, writes that 2019 marks “the year Chinese investors went all in on the continent’s startup scene” — particularly its fintech projects. Why?

“The continent’s 1.2 billion people represent the largest share of the world’s unbanked and underbanked population — which makes fintech Africa’s most promising digital sector,” Bright notes. “In previous years, the country’s interactions with African startups were relatively light compared to deal-making on infrastructure and commodities. Chinese actors investing heavily in African mobile consumer platforms lends to looking at new data-privacy and security issues for the continent.”

Active Chinese investors in Africa include Hillhouse Capital, Meituan-Dianping, GaoRong, Source Code Capital, SoftBank Ventures Asia, BAI, Redpoint, IDG Capital, Sequoia China, Crystal Stream Capital, GSR Ventures, Chinese mobile-phone maker Transsion and NetEase .

Here’s more of TechCrunch’s recent coverage of Africa startup activity:

It was a short week (Happy Thanksgiving, by the way). But here’s a quick look at the top deals of the last few days.

Last week, Facebook announced it was buying Beat Games, the game studio behind Beat Saber, a rhythm game that’s equal parts Fruit Ninja and Guitar Hero. Heard of the company? Maybe if you’re a gamer, but if you’re readying this newsletter because of your interest in VC, this company may not have come across your radar.

Why? It’s one of virtual reality’s biggest successes today, but it’s just an eight-person team with no funding.

“I’m really proud that we were able to build the company with this mindset of making decisions based on what is good for the game and not what is the most profitable thing,” Beat Games CEO told TechCrunch earlier this year. Read about Facebook’s acquisition here and an in-depth profile of the small team here.

If you like this newsletter, you will definitely enjoy Equity, which brings the content of this newsletter to life — in podcast form! Join myself and Equity co-host Alex Wilhelm every Friday for a quick breakdown of the week’s biggest news in venture capital and startups.

This week, we discussed Weekend Fund’s new vehicle, Cocoon’s new friend-tracking app and the unfortunate demise of a startup called Omni. You can listen here.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

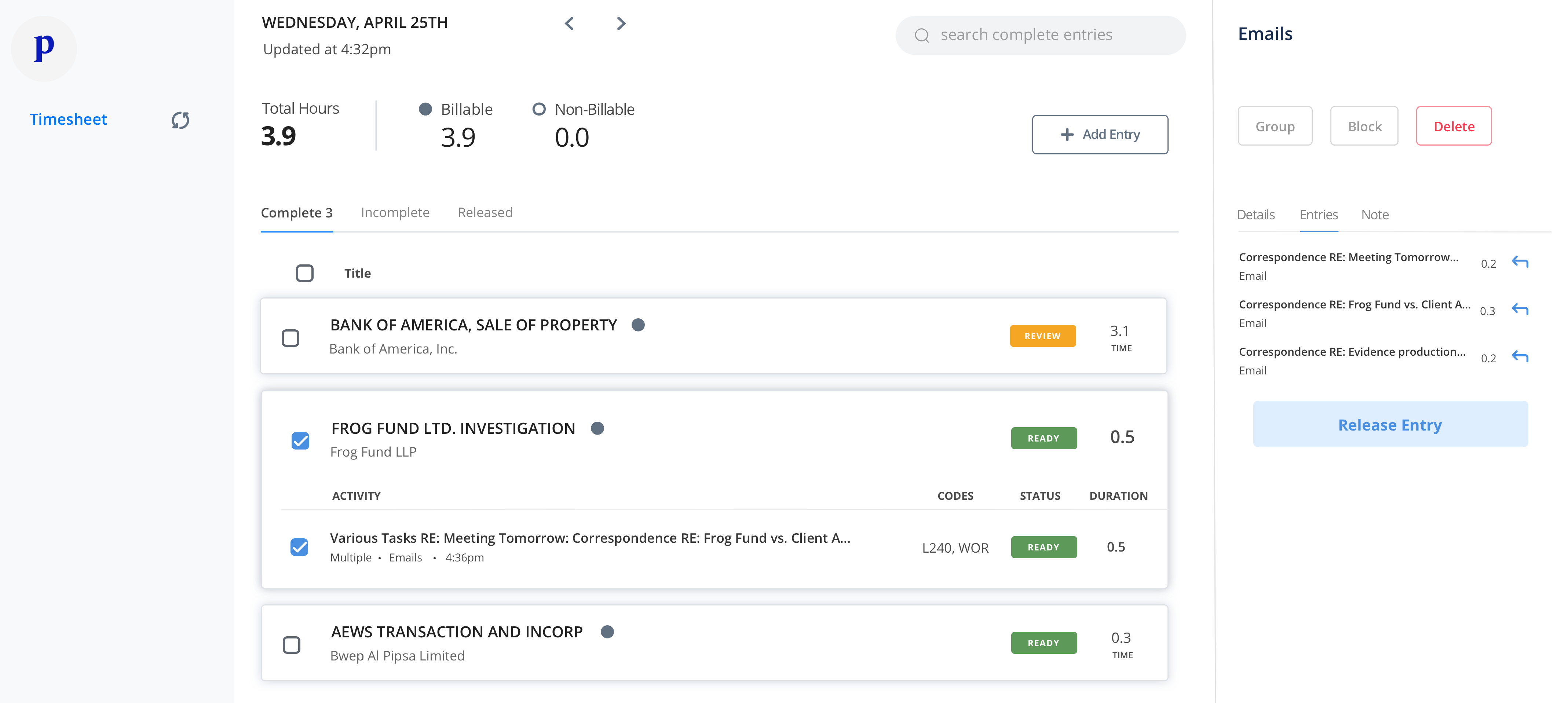

Counting billable time in six-minute increments is the most annoying part of being a lawyer. It’s a distracting waste. It leads law firms to conservatively under-bill. And it leaves lawyers stuck manually filling out timesheets after a long day when they want to go home to their families.

Life is already short, as Ping CEO and co-founder Ryan Alshak knows too well. The former lawyer spent years caring for his mother as she battled a brain tumor before her passing. “One minute laughing with her was worth a million doing anything else,” he tells me. “I became obsessed with the idea that we spend too much of our lives on things we have no need to do — especially at work.”

That’s motivated him as he’s built his startup Ping, which uses artificial intelligence to automatically track lawyers’ work and fill out timesheets for them. There’s a massive opportunity to eliminate a core cause of burnout, lift law firm revenue by around 10% and give them fresh insights into labor allocation.

Ping co-founder and CEO Ryan Alshak (Image Credit: Margot Duane)

That’s why today Ping is announcing a $13.2 million Series A led by Upfront Ventures, along with BoxGroup, First Round, Initialized and Ulu Ventures. Adding to Ping’s quiet $3.7 million seed led by First Round last year, the startup will spend the cash to scale up enterprise distribution and become the new timekeeping standard.

“I was a corporate litigator at Manatt Phelps down in LA and joke that I was voted the world’s worst timekeeper,” Alshak tells me. “I could either get better at doing something I dreaded or I could try and build technology that did it for me.”

The promise of eliminating the hassle could make any lawyer who hears about Ping an advocate for the firm buying the startup’s software, like how Dropbox grew as workers demanded easier file sharing. “I’ve experienced first-hand the grind of filling out timesheets,” writes Initialized partner and former attorney Alda Leu Dennis. “Ping takes away the drudgery of manual timekeeping and gives lawyers back all those precious hours.”

Traditionally, lawyers have to keep track of their time by themselves down to the tenth of an hour — reviewing documents for the Johnson case, preparing a motion to dismiss for the Lee case, a client phone call for the Sriram case. There are timesheets built into legal software suites like MyCase, legal billing software like TimeSolv and one-off tools like Time Miner and iTimeKeep. They typically offer timers that lawyers can manually start and stop on different devices, with some providing tracking of scheduled appointments, call and text logging, and integration with billing systems.

Ping goes a big step further. It uses AI and machine learning to figure out whether an activity is billable, for which client, a description of the activity and its codification beyond just how long it lasted. Instead of merely filling in the minutes, it completes all the logs automatically, with entries like “Writing up a deposition – Jenkins Case – 18 minutes.” Then it presents the timesheet to the user for review before they send it to billing.

The big challenge now for Alshak and the team he’s assembled is to grow up. They need to go from cat-in-sunglasses logo Ping to mature wordmark Ping. “We have to graduate from being a startup to being an enterprise software company,” the CEO tells me. That means learning to sell to C-suites and IT teams, rather than just build a solid product. In the relationship-driven world of law, that’s a very different skill set. Ping will have to convince clients it’s worth switching to not just for the time savings and revenue boost, but for deep data on how they could run a more efficient firm.

Along the way, Ping has to avoid any embarrassing data breaches or concerns about how its scanning technology could violate attorney-client privilege. If it can win this lucrative first business in legal, it could barge into the consulting and accounting verticals next to grow truly huge.

With eager customers, a massive market, a weak status quo and a driven founder, Ping just needs to avoid getting in over its heads with all its new cash. Spent well, the startup could leap ahead of the less tech-savvy competition.

Alshak seems determined to get it right. “We have an opportunity to build a company that gives people back their most valuable resource — time — to spend more time with their loved ones because they spent less time working,” he tells me. “My mom will live forever because she taught me the value of time. I am deeply motivated to build something that lasts . . . and do so in her name.”

Powered by WPeMatico

Kandji, a new Apple MDM solution that promises to go far beyond Apple’s base MDM protocol and other solutions on the market, emerged from stealth today with a $3.375 million seed investment. The product is also publicly available for the first time starting today.

The round, which closed in March, was led by First Round Capital with help from Webb Investment Network, Lee Fixel, John Glynn and other unnamed investors.

Company co-founder and CEO Adam Pettit says the company’s founders have a deep knowledge in Apple. They all worked at Apple before leaving to run an Apple IT consultancy for more than 10 years.

He said that while they were at the consultancy, they developed a proprietary stack of tools to help with highly sophisticated Apple device deployments at large organizations, and it occurred to them that there was an unserved market opportunity to turn that knowledge into a new product.

Two years ago they sold the consultancy, took that knowledge and built Kandji from the ground up. Pettit says the new product gives customers access to a set of management tools that they would have charged six figures to implement at that their old firm.

One of the key differentiators between Kandji and other MDM solutions, or even Apple’s base MDM functionality, is a set of one-click compliance tools. “We’re the only product that has almost 200 of these one-click policy frameworks we call parameters. So an organization can go in and browse by compliance framework, or we have pre-built templates for companies that don’t necessarily have a specific compliance mandate in mind,” he said.

The parameters have all of the tools built-in to automatically deploy a set of policies related to a given compliance framework without having to go through and manually set all of those different switches yourself. On the flip side, if you want to get granular and create your own parameters, you can do that too.

He says one of the reasons he and his partners were willing to give up the big-dollar consultancy was because they saw a huge opportunity for firms that couldn’t afford those kind of services, but still had relatively large Apple device deployments. “I mean there’s a big need outside of just the specific kind of sophisticated compliance work we would do [at our previous firm]. We saw this big need in general for an Apple MDM solution like ours,” he said.

After selling their previous firm, the founders bootstrapped for a year while they developed the initial version of Kandji before seeking funding. Today, the company has 16 employees and a set of initial customers that have been testing the product.

Powered by WPeMatico

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on revenue-based investing VC that will hit on:

A new wave of revenue-based investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt.

I’ve been a traditional equity VC for 8 years, and I’m researching new business models in venture capital. As I’ve learned about this model, I’ve been impressed by how these venture capitalists are accomplishing a major social impact goal… without even trying to.

Many are reporting that they’re seeing a more diverse pool of applicants than traditional equity VCs — even though virtually none have a particular focus on women or underrepresented founders. In addition, their portfolios look far more diverse than VC industry norms.

For context, revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance. For more background, see “Revenue-based investing: A new option for founders who care about control“.

I contacted every RBI venture capital investor I could identify, and learned:

By contrast, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data says that in fact you’re better off investing in women.

Paul Graham href=”http://www.paulgraham.com/bias.html”> observes, “many suspect that venture capital firms are biased against female founders. This would be easy to detect: among their portfolio companies, do startups with female founders outperform those without?

A couple months ago, one VC firm (almost certainly unintentionally) published a study showing bias of this type. First Round Capital found that among its portfolio companies, startups with female founders outperformed those without by 63%.”

Image via Getty Images / runeer

Why are RBI investors investing disproportionately in women & underrepresented founders, and vice versa: why do these founders approach RBI investors?

I’d argue it’s not that RBI is so unbiased and attractive; it’s that traditional equity VC is biased structurally against some women and underrepresented founders.

The Boston Consulting Group and MassChallenge, a US-based global network of accelerators, partnered to study why “women-owned startups are a better bet”. Through their analysis and interviews, BCG identified three primary reasons why female founders are less likely to receive VC funds.

The study used multivariate regression analysis to control for education levels and pitch quality to conclude that gender was a statistically significant factor. I argue that these 3 reasons are much less applicable for RBI investors than for conventional VCs.

Traditional equity VCs are looking for high-risk, high-reward, “swing for the fences” models. The founders of such companies inherently are taking financial risk, reputational risk, and career risk.

Paul Graham, co-founder of Y Combinator, said, “few successful founders grew up desperately poor.” Ricky Yean, a serial founder, agrees: “building and sustaining a company that is “designed to grow fast” is especially hard if you grew up desperately poor”.

Most of the founders of the paradigmatic VC home runs were privileged: male, cisgender, well-educated, from affluent families, etc. Think Bill Gates and Mark Zuckerberg .

That privilege makes it easier for them to take very high risk. The average person, worried about students loans and long term employability, quite rationally is less likely to take the huge risk of founding a company. It’s far safer to just get a job.

Investors who back diverse teams can win much higher returns than the industry norm. Both RBI investors and the founders they back will hopefully benefit from this pattern.

Note that none of the lawyers quoted or I are rendering legal advice in this article, and you should not rely on our counsel herein for your own decisions. I am not a lawyer. Thanks to the experts quoted for their thoughtful feedback.

Powered by WPeMatico

Growing D2C brands face an interesting challenge. While they’ve eliminated much of the hassle of a physical storefront, they must still deal with all the complications involved in managing inventory and manufacturing and shipping a physical product to suppliers.

Anvyl, with a fresh $9.3 million in Series A funding, is looking to jump in and make a difference for those brands. The company, co-founded by chief executive Rodney Manzo, is today announcing the raise, led by Redpoint Ventures, with participation from existing investors First Round Capital and Company Ventures. Angel investors Kevin Ryan (MongoDB and DoubleClick), Ben Kaufman (Quirky and Camp) and Dan Rose (Facebook) also participated in the round.

Manzo hails from Apple, where with $300 million in spend to manage logistics and supply chain he was still operating in an Excel spreadsheet. He then went to Harry’s, where he shaved $10 million in cash burn in his first month. He says himself that sourcing, procurement and logistics are in his DNA.

Which brings us to Anvyl. Anvyl looks at every step in the logistics process, from manufacture to arrival at the supplier, and visualizes that migration in an easy-to-understand UI.

The difference between Anvyl and other supply chain logistics companies, such as Flexport, is that Anvyl goes all the way to the very beginning of the supply chain: the factories. The company partners with factories to set up cameras and sensors that let brands see their product actually being built.

“When I was at Apple, I traveled for two years at least once a month to China and Japan just to oversee production,” said Manzo. “To oversee production, you essentially have to be boots on the ground and eyes in the factory. None of our brands have traveled to a factory.”

On the other end of the supply chain, Anvyl lets brands manage suppliers, find new suppliers, submit RFQs, see cost breakdowns and accept quotes.

The company also looks at each step in between, including trucks, trains, boats and planes so that brands can see, in real time, their products go from being manufactured to delivery.

Anvyl charges brands a monthly fee using a typical SaaS model. On the other end, Anvyl takes a “tiny percentage” of goods being produced within the Anvyl marketplace. The company declined to share actual numbers around pricing.

This latest round brings Anvyl’s total funding to $11.8 million. The company plans to use the funding toward hiring in engineering and marketing, and grow its consumer goods customer base.

Powered by WPeMatico

Startups depend on the angel lifecycle. A few flush post-exit individuals put the first cash into a fresh venture. With some skill and plenty of luck, the early team grows the company into a big success. It sells or goes public and those team members earn a fortune. They then pay it forward by investing in the next generation of startups.

If they hoard their spoils they starve the early-stage ecosystem or leave founders stuck with dumb money from non-strategic financiers. If they redistribute their winnings, they can influence startup culture by deciding what, and more importantly, who gets funding.

But how does a co-founder or VP learn to be a mini-VC? That’s the goal of First Round Capital’s Angel Track, a free three-month workshop series in San Francisco and New York for learning how to source, vet, close, and support angel investments.

A scene from Angel Track’s first cohort

Every two weeks, an expert on some part of the investing process like finding deals or interviewing founders talks to the class, does Q&A, and then leaves the group to openly discuss what they learned and how to use it. Angel Track sessions have been tought by some of the smartest people in the valley like growth master Elad Gil, #ANGELS founding partner and former Twitter VP of corp dev Jessica Verrilli, and Precursor Ventures managing partner Charles Hudson.

Hundreds of startup execs apply for the 15 spots on each coast. After two classes in SF and one in NYC, today First Round unveiled its recently-graduated third cohort from programs in both cities. Those include Lucy Zhang who sold Facebook her chat startup Beluga that became the foundation of Messenger, and Mented Cosmetics co-founder and CEO KJ Miller. By the end of the program they’re taking joint pitch meetings from startups, showing each other the best questions to ask.

As with Y Combinator, it’s as much about the fellowship between new investors as the education. “It’s both a community and a masterclass” says First Round general partner Hayley Barna who oversees the NYC Angel Track. “It’s about bringing a talented group of emerging angels together to build a productive cohort of collaborators.”

She says diversity and inclusion is a big goal of the program, and it features 50% women and 20% underrepresented minorities. Being rich is not a pre-requisite. Barna declares “We’re not pulling in the bankers and the traders doing angel investing as a side-hustle.”

LOS ANGELES, CA – MARCH 29: Confetti falls as Lyft CEO Logan Green (C) rings the Nasdaq opening bell celebrating the company’s initial public offering (IPO) on March 29, 2019 in Los Angeles, California. The ride hailing app company’s shares were initially priced at $72. (Photo by Mario Tama/Getty Images)

After a slew of big 2019 IPOs from Uber, Lyft, Pinterest, Slack, and Zoom, there are plenty of newly-minted potential angels for First Round to teach. The venture firm benefits by building a cadre of co-investors or alternative backers for deals it vets, and through added visibility into the next top fundraises. Unlike some VC scout programs, there’s no formal obligation to send opportunities to First Round or pledge funding alongside it. That keeps it appealing to future investors that innovation hubs need to keep the circle of life flowing.

![]()

“A lot of angel investors that got their start in the mid-to late 2000s, they’re almost all fund managers now. They went from angels or super angels to venture investors” First Round partner Brett Berson tells me. “There haven’t been a lot of people who’ve come in and filled that gap”, which could stunt the ecosystem’s growth. Graduates ramp up their angel investing while often staying in their operating roles, though some like former Pinterest head of culture Cat Lee who became a partner at Maveron turn investing into their day job.

First Round VP Ben Cmejla who helped launch the program explains that “Some people are doing it for the financial return. Some people want access to new ideas and are curious. Some people have a specific type of community they want to support with their investments.”

Becoming a successful angel means a lot more than evaluating term sheets. Just like how ideas are a dime a dozen and it’s about who can execute, fundraises are frequent but getting into the right ones takes hard work. First Round focuses on many of the soft skills required to win. Participants receive mentorship on how to:

How to approach the delicate power balance of meetings with entrepreneurs can be especially tricky, so I spoke at length with First Round’s Phin Barnes about the session he teaches on founder interviews. I wanted to get a taste for what it’d be like in the classroom, despite First Round declining to let me attend the real thing. Turns out having a journalist in the room can disrupt a safe learning environment for budding angels.

First Round partner Phin Barnes

“Investing is a sell-side product” Barnes stresses. “Capital is a commodity, especially in this market. What you’re saying with a term sheet is that you think the founder’s equity is worth more than your dollars.” That means investors have to close the value gap with sweat.

Barnes gives me what he calls the ‘chocolate soufflé or brownies’ scenario. “The danger of being a smart, talented executive or entrepreneur is that when a founder talks to you about sugar and flour and butter, you start imagining a molten lava soufflé cake you’d build with the ingredients. You invest, and then the founder comes back with a tray of brownies. ‘That’s not what I thought I invested in!’”

The mistake comes in envisioning what you’d do rather than really listening to the founder — the one who’s cooking. Instead of trying to hijack the roadmap or being disappointed by the direction, angels need to help make those brownies as tasty as possible. That means entering into interviews with an open mind.

“You should be positively inclined to invest and have some critical questions. If you don’t think you should invest, you shouldn’t have the meeting in the first place” Barnes explains. “You want to hold that perspective loosely and as new information comes to light, you want to check ‘Am I still interested?’ By the end you want to know what you don’t know, and the open questions you need to answer to validate your hypothesis.”

The four main areas of evaluation are:

The market — Why does this category of product need to exist? What would the world look like if they dominate the category? Can they clearly explain to a five-year old the problem they’re trying to solve? What’s their contrarian thinking? And what motivation will keep them persevering to address the problem despite setbacks and opportunity cost?

The product — Is addressing this specific customer problem unique and defensible? It’s less about if the product is good or bad, or should the button be red or blue. It’s more about how the founder took the inputs and made the decision and how they process information. Have them walk you through the go-to-market plan and see how they shift between high-level strategy and ground-level tactics.

The team — Do they have on-paper talent like PhDs or experience? Can they iterate quickly? You have to weed out victims and look for people who are learners that evolve when faced with adversity. Do your homework on who they are before so you can dig deeper into how they tick. Ask how they show trust in their team and how they get their team to trust them. Have them tell you about the most important thing that happened at the company in the last week to understand their priorities and emotional connection to the process.

The relationship with the founder — Investors need to ask what the best way to work with them is, and what founders are looking for in support from an investor. Do they want a hands-off investor who only chimes in when summoned, or do they expect frequent co-building sessions? Do they need more help accessing a bigger network for hiring and partnerships, or industry-specific expertise to navigate complex decisions?

“We have two roles. We interview and then we coach” Barnes says, providing tips for both. “The very best questions are open-ended. They start with a how/what/why and end with a question mark. Double-barreled questions are terrible. Ask them what would you do, and stop. Get comfortable with silence. They’ll usually fill the silence with something off-script that reveals a deeper truth.” Only once has a founder asked Barnes ‘are you ok?’ in response to his inquisitive stare.

Being able to summarize what you’ve learned lets you quickly cross-check your assumptions with the founder and get helpful corrections. That helps you figure out what questions you still need to ask and keep a diligent list of what you’ll need to research after.

When it comes to giving an answer on whether you’ll invest, “Second best to a quick yes is a quick no with a strong point of view and information for the entrepreneur. The worst is ghosting people. 90% of people operate that way but that’s not the way to do it” Barnes emphasizes. “If you walk out without a yes, no, or what to learn more about in specific detail, you’ve failed as an investor and wasted the time of the entrepreneur.”

“It was like the perfect mix of your favorite college seminar and a super practical apprenticeship” says Ariana Poursartip, the VP of product for fintech startup Petal who was in the first NYC Angel Track class. “I came away with a better sense of my personal investing approach, and a community of fellow angel investors who I’ll continue to learn from for years.”‘

Fostering better educated angels is crucial for enabling founders. “Dumb money” from investors without expertise in a relevant space, connections they’ll leverage to help, or an understanding of what startups need can be dangerous. It can lead founders to raise more but inefficient capital and make slower progress that puts them at risk of a future down-round that can trigger a startup death spiral.

First Round’s Angel Track cohort 3

First Round is far from the only one trying to fill the angel gap. “Initiatives like Spearhead, YC’s Startup Investor School, and scout programs help lower the barrier to entry for many people who will be terrific and helpful investors for startups” says Cmejla. Sequoia, General Catalyst, Village Global and more run their own scout networks. There are some questionable programs out there too, though, like Venture University which charges from $4,000 to $65,000 for its programs that require students to source deals in exchange for a hazy profit-sharing agreement.

Cmejla insists “It isn’t about providing the capital, a short crash course, or a path to becoming a full-time VC, but about building a durable community that members can lean on and lean into as they level up.” Instead, First Round scores a way to connect founders it funds with relevant angels from its classes. That incentivizes the firm to teach savvy etiquette. Barna warns “You want to be thorough, but if you’re putting in a small check, you can’t ask founders to jump through too many hoops . . . and spend five hours just to get that dinky paycheck.”

Cmejla insists “It isn’t about providing the capital, a short crash course, or a path to becoming a full-time VC, but about building a durable community that members can lean on and lean into as they level up.” Instead, First Round scores a way to connect founders it funds with relevant angels from its classes. That incentivizes the firm to teach savvy etiquette. Barna warns “You want to be thorough, but if you’re putting in a small check, you can’t ask founders to jump through too many hoops . . . and spend five hours just to get that dinky paycheck.”

Past Angel Track participants like Poursartip and Instacart VP of growth Bengaly Kaba tell me they wish the program got them spending more time together both during and after the class, which could spur deeper alliances. “Currently the program ends and there is no formal programming to keep the alumni cohorts engaged and connected” Kaba notes. Many already back startups brought to the class by their peers. Still, Square Cash app product lead Ayo Omojola wanted a stronger structure like perhaps a syndicate so cohort-mates could do more investing together.

What they all cited was the massive value of learning to codify what they’re looking for and what they bring to the table. Kaba highlighted how he enjoyed “Hearing how Elad Gil, [Floodgate co-founding partner] Ann Muira-Ko, Charles Hudson and other guest speakers defined their investment theses around macro trends, industry specific insights, and founder traits.”

When the lock-ups expire on recent IPOs and employees start getting liquidity, “you’re going to see a whole new generation of investors get going over the next couple of years” says Berson.

Not every company spawns the same quality of investor, though. Companies like Uber that empower less-senior team members as the ride sharing company does with regional general managers tend to develop talent with the self-direction and conviction to be great angels. Looking back, you similarly see more angels and founders emerging from more decentralized Google than top-down Apple.

As software eats the world, unicorns proliferate, and the proceeds of tech’s winning streak are spread wide, more and more people will be ready to write angel checks. “It will most likely materially accelerate over the next 12-24 months” Berson concludes. Those without the skills could squander what they’ve earned. Angels who know what makes them special and can evaluate startups without getting swept up in the hype will crown the queens of tomorrow.

Powered by WPeMatico

Slack wants to be the new operating system for teams, something it has made clear on more than one occasion, including in its recent S-1 filing. To accomplish that goal, it put together an in-house $80 million venture fund in 2015 to invest in third-party developers building on top of its platform.

Weeks ahead of its direct listing on The New York Stock Exchange, it continues to put that money to work.

Troops is the latest to land additional capital from the enterprise giant. The New York-based startup helps sales teams communicate with a customer relationship management tool plugged directly into Slack. In short, it automates routine sales management activities and creates visibility into important deals through integrations with employee emails and Salesforce.

Troops founder and chief executive officer Dan Reich, who previously co-founded TULA Skincare, told TechCrunch he opted to build a Slackbot rather than create an independent platform because Slack is a rocket ship and he wanted a seat on board: “When you think about where Slack will go in the future, it’s obvious to us that companies all over the world will be using it,” he said.

Troops has raised $12 million in Series B funding in a round led by Aspect Ventures, with participation from the Slack Fund, First Round Capital, Felicis Ventures, Susa Ventures, Chicago Ventures, Hone Capital, InVision founder Clark Valberg and others. The round brings Troops’ total raised to $22 million.

Launched in 2015 by New York tech veterans Reich, Scott Britton and Greg Ratner, the trio weren’t initially sure of Slack’s growth trajectory. It wasn’t until Slack confirmed its intent to support the developer ecosystem with a suite of developer tools and a fund that the team focused its efforts on building a Slackbot.

“People sometimes thought of us, at least in the early days, as a little bit crazy,” Reich said. “But now Slack is the fastest-growing SaaS company ever.”

“We think the biggest opportunity in the [enterprise SaaS] category is going to be tools oriented around the customer-facing employee (CRM), and that’s where we are innovating,” he added.

Troops’ tools are helpful for any customer-facing team, Reich explains. Envoy, WeWork, HubSpot and a few hundred others are monthly paying subscribers of the tool, using it to interact with their CRM in a messaging interface and to receive notifications when a deal has closed. Troops integrates with Salesforce, so employees can use it to search records, schedule automatic reports and celebrate company wins.

Slack, in partnership with a number of venture capital funds, including Accel, Kleiner Perkins and Index, has also deployed capital to a number of other startups, like Lattice, Drafted and Loom.

With Slack’s direct listing afoot, the Troops team is counting on the imminent and long-term growth of the company’s platform.

“We think it’s still early days,” Reich said. “In the future, we see every company using something like Troops to manage their day-to-day.”

Powered by WPeMatico