funding

Auto Added by WPeMatico

Auto Added by WPeMatico

Vouch, a provider of business insurance to startups and high-growth companies, announced today it has raised $90 million in new funding.

The $90 million figure was raised across two rounds: a $60 million Series C co-led by SVB Capital (a subsidiary of Silicon Valley Bank) and Ribbit Capital that values the company at $550 million, and a previously unannounced $30 million Series B1 led by Redpoint Ventures.

With the latest financing, San Francisco-based Vouch has now raised a total of $160 million since its 2018 inception. Other investors include Allegis Group, Sound Ventures and SiriusPoint.

While there are many insurance technology companies out there that serve consumers, there are far fewer that offer it to companies, much less startups. Vouch describes itself as “a new kind of insurance platform” for startups that offers fully digital, “tailored coverage that takes minutes to activate.”

Over the past year, Vouch has seen impressive growth. The company declined to reveal hard revenue figures, but said it saw “7x” increase in its customer base year over year and currently protects over $5.7 billion in risk across thousands of policies. Today, Vouch has more than 1,600 clients, including Pipe, Middesk, Neighbor and Routable. It is also the “preferred” business insurance provider to the customers of Silicon Valley Bank, Brex, Carta and WeWork. Y Combinator too also refers Vouch to its portfolio companies.

To Vouch co-founder and CEO Sam Hodges, the ability to attract some of the highest-profile businesses in the startup world speaks to the company’s understanding of the startup ecosystem.

“It’s our responsibility to meet startup founders where they are, and give startups flexibility as they navigate changing laws, regulations and the virtual and physical locations of their businesses,” he said.

Like many other companies, Vouch had to shift its model during the pandemic to adapt to the different types of emerging risks businesses have faced. For example, last year, Vouch saw a change in where its startup clients’ teams were distributed. Before the pandemic, nearly 30% of the teams were remote. During the pandemic, that figure has shifted to over 53%. As a result, Vouch developed a broader range of insurance coverages to adapt to the “new normal.”

Included in its new line of proprietary products and services aimed at startups are: work from anywhere coverage, broader cyber coverages and embedded insurance. It also expanded its underwriting capabilities to serve early-stage to growth-market startups.

In particular, the work from anywhere coverage is in direct response to the pandemic-related shift in remote work and can insure up to $500,000 per occurrence and can include a specified property owned by a startup regardless of the location of that property.

One major differentiator for Vouch, said Hodges, is that it is now the only business insurance provider for startups that has its own insurance carrier, which means the company backs its own policies.

“This capability means we have a lot of control over how we build and underwrite our policies — which translates into superior coverage and a better experience for our clients,” he said.

Hodges co-founded Vouch with Travis Hedge three years ago after seeing how challenging it could be for a company to get the business insurance it needs to start and then scale.

The goal is to make it as easy as possible to onboard new customers and personalize the coverage as much as possible based on each company’s needs based on what they do, their customer base, stage of growth and the founder’s threshold for risk.

“A typical client can get a quote and bind their coverage online in under 10 minutes, without any phone calls or paperwork,” he told TechCrunch. “Vouch also has many coverage features that are uniquely geared for startups. For example, our directors and officers coverage includes a cap table coverage feature meant specifically to protect startups.”

Vouch looks at startups that need business insurance on a case by case basis, Hodges added.

For example, it asks questions like, “Does an e-commerce company handle a very limited amount of client-sensitive information?” If so, it could make sense that it has a lower cyber insurance coverage limit and pay less for its policy.

Conversely, if a startup is trying to raise money, it might need to invest more in Vouch’s directors and officers insurance to make sure it is covered should disputes arise in the future.

Looking ahead, Hodges said the new capital would go toward continued investment in technical capabilities, an expansion of its product offerings, more hiring and building embedded insurance for its partners.

With regard to the embedded capabilities, within the next 12 months, all of the company’s partners’ customers will be able to purchase Vouch insurance directly from those partners’ websites. Vouch’s headcount has more than doubled, from 55 employees in September 2020 to 125 full-time employees presently, and Hodges expects that will continue to grow.

Greg Becker, president and CEO of SVB Financial Group, said that Vouch’s mission aligns with SVB’s in that they both aim to “empower the innovation economy.”

“That’s what Vouch is doing today, helping startups and tech innovators mitigate their risks as they grow,” he wrote via email. “We are proud to co-lead Vouch’s latest funding round to give startups access to the insurance they need as they add headcount, increase their customer base, or raise funding rounds of their own.”

Powered by WPeMatico

Media technology company Amagi announced Friday $100 million to further develop its cloud-based SaaS technology for broadcast and connected televisions.

Accel, Avataar Ventures and Norwest Venture Partners joined existing investor Premji Invest in the funding round, which included buying out stakes held by Emerald Media and Mayfield Fund. Nadathur Holdings continues as an existing investor. The latest round gives Amagi total funding raised to date of $150 million, Baskar Subramanian, co-founder and CEO of Amagi, told TechCrunch.

Bangalore-based Amagi provides cloud broadcast and targeted advertising software so that customers can create content that can be created and monetized to be distributed via broadcast TV and streaming TV platforms like The Roku Channel, Samsung TV Plus and Pluto TV. The company already supports more than 2,000 channels on its platform across over 40 countries.

“Video is a complex technology to manage — there are large files and a lot of computing,” Subramanian said. “What Amagi does is enable a content owner with zero technology knowledge to simplify that complex workflow and scalable infrastructure. We want to make it easy to plug in and start targeting and monetizing advertising.”

As a result, Amagi customers see operational cost savings on average of up to 40% compared to traditional delivery models and their ad impressions grow between five and 10 times.

The new funding comes at a time when the company is experiencing rapid growth. For example, Amagi grew 30 times in the United States alone over the past few years, Subramanian said. Amagi commands an audience of over 2 billion people, and the U.S. is its largest market. The company also sees growth potential in both Latin America and Europe.

In addition, in the last year, revenue grew 136%, while new customer year over year growth was 44%, including NBCUniversal — Subramanian said the Tokyo Olympics were run on Amagi’s platform for NBC, USA Today and ABS-CBN.

As more of a shift happens with video content being developed for connected television experiences, which he said is a $50 billion market, the company plans to use the new funding for sales expansion, R&D to invest in the company’s product pipeline and potential M&A opportunities. The company has not made any acquisitions yet, Subramanian added.

In addition to the broadcast operations in New Delhi, Amagi also has an innovation center in Bangalore and offices in New York, Los Angeles and London.

“Consumer behavior and infrastructure needs have reached a critical mass and new companies are bringing in the next generation of media, and we are a large part of that growth,” Subramanian said. “Sports will come on quicker, while live news and events are going to be one of the biggest growth areas.”

Shekhar Kirani, partner at Accel, said Amagi is taking a unique approach to enterprise SaaS due to that $50 billion industry shift happening in video content, where he sees half of the spend moving to connected television platforms quickly.

Some of the legacy players like Viacom and NBCUniversal created their own streaming platforms, where Netflix and Amazon have also been leading, but not many SaaS companies are enabling the transition, he said.

When Kirani met Subramanian five years ago, Amagi was already well funded, but Kirani was excited about the platform and wanted to help the company scale. He believes the company has a long tailwind because it is saving people time and enabling new content providers to move faster to get their content distributed.

“Amagi is creating a new category and will grow fast,” Kirani added. “They are already growing and doubling each year with phenomenal SaaS metrics because they are helping content providers to connect to any audience.

Powered by WPeMatico

Snyk, the Boston-based late-stage startup that is trying to help developers deliver more secure code, announced another mega-round today. This one was for $530 million, with $300 million in new money and $230 million in secondary funding, the latter of which is to help employees and early investors cash in some of their stock options.

The long list of investors includes an interesting mix of public investors, VC firms and strategics. Sands Capital Ventures and Tiger Global led the round, with participation from new investors Baillie Gifford, Koch Industries, Lone Pine Capital, T. Rowe Price and Whale Rock Capital Management. Existing investors also came along for the ride, including Accel, Addition, Alkeon, Atlassian Ventures, BlackRock, Boldstart Ventures, Canaan Partners, Coatue, Franklin Templeton, Geodesic Capital, Salesforce Ventures and Temasek.

This round brings the total raised in funding to $775 million, excluding secondary rounds, according to the company. With secondary rounds, it’s up to $1.3 billion, according to Crunchbase data. The company has been raising funds at a rapid clip (note that the last three rounds include the Snyk money plus secondary rounds):

While the company wouldn’t share specific revenue figures, it did say that ARR has grown 158% YoY; given the confidence of this list of investors and the valuation, it would suggest the company is making decent money.

Snyk CEO Peter McKay says that the additional money gives him flexibility to make some acquisitions if the right opportunity comes along, what companies often refer to as “inorganic” growth. “We do believe that a portion of this money will be for inorganic expansion. We’ve made three acquisitions at this point and all three have been very, very successful for us. So it’s definitely a muscle that we’ve been developing,” McKay told me.

The company started this year with 400 people and McKay says they expect to double that number by the end of this year. He says that when it comes to diversity, the work is never really done, but it’s something he is working hard at.

“We’ve been able to build a lot of good programs around the world to increase that diversity and our culture has always been inclusive by nature because we’re highly distributed.” He added, “I’m not by any means saying we’re even remotely close to where we want to be. So I want to make that clear. There’s a lot we still have to do,” he said.

McKay says that today’s investment gives him added flexibility to decide when to take the company public because whenever that happens it won’t have to be because they need another fundraising event. “This raise has allowed us to set up with strong, highly reputable public investors, and it gives us the financial resources to pick the timing. We are in control of when we do it and we will do it when it’s right,” he said.

Powered by WPeMatico

Relationships ultimately close deals, but long-term relationships come with a lot of baggage, i.e. email interactions, documents and meetings.

Affinity wants to take what Ray Zhou, co-founder and CEO, refers to as “data exhaust,” all of those daily interactions and communications, and apply machine learning analysis and provide insights on who in the organization has the best chance of getting that initial meeting and closing the deal.

Today, the company announced $80 million in Series C funding, led by Menlo Ventures, which was joined by Advance Venture Partners, Sprints Capital, Pear Ventures, Sway Ventures, MassMutual Ventures, Teamworthy and ECT Capital Partners’ Brian N. Sheth. The new funding gives the company $120 million in total funding since it was founded in 2014.

Affinity, based in San Francisco, is focused on industries like investment banking, private equity, venture capital, consulting and real estate, where Zhou told TechCrunch there aren’t customer relationship management systems or networking platforms that cater to the specific needs of the long-term relationship.

Stanford grads Zhou and co-founder Shubham Goel started the company after recognizing that while there was software for transactional relationships, there wasn’t a good option for the relationship journeys.

He cites data that show up to 90% of company profiles and contact information living in traditional CRM systems are incomplete or out of date. This comes as market researcher Gartner reported the global CRM software market grew 12.6% to $69 billion in 2020.

“It is almost bigger than sales,” Zhou said. “Our worldview is that relationships are the biggest industries in the world. Some would disagree, but relationships are an asset class, they are a currency that separates the winners from the losers.”

Instead, Affinity created “a new breed of CRM,” Zhou said, that automates the inputting of that data constantly and adds information, like revenue, staff size and funding from proprietary data sources, to assign a score to a potential opportunity and increase the chances of closing a deal.

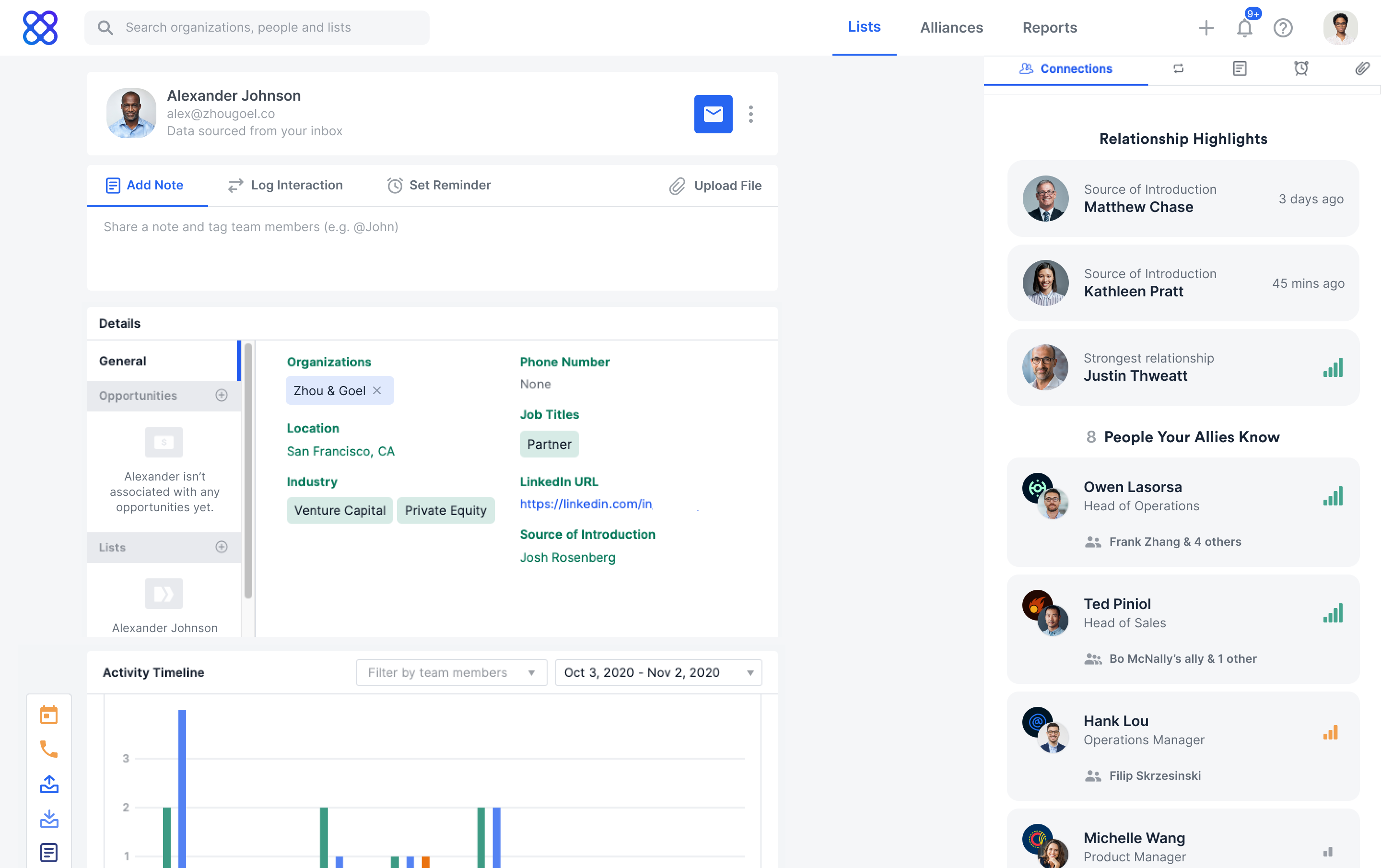

Affinity people profile. Image Credits: Affinity

He intends to use the new funding to expand sales, marketing and engineering to support new products and customers. The company has 125 employees currently; Zhou expects to be over 200 by next year.

To date, the company’s platform has analyzed over 18 trillion emails and 213 million calendar events and currently drives over 500,000 new introductions and tracks 450,000 deals per month. It also has more than 1,700 customers in 70 countries, boasting a list that includes Bain Capital Ventures, Kleiner Perkins, SoftBank Group, Nike, Qualcomm and Twilio.

Tyler Sosin, partner at Menlo Ventures, said he met Zhou and Goel at a time when the firm was looking into CRM companies, but it wasn’t until years later that Affinity came up again when Menlo itself wanted to work with a more modern platform.

As a user of Affinity himself, Sosin said the platform gives him the data he cares about and “removes the manual drudgery of entry and friction in the process.” Affinity also built a product that was intuitive to navigate.

“We have always had an interest in getting CRMs to the next generation, and Affinity is defining itself in a new category of relationship intelligence and just crushing it in the private capital markets,” he said. “They are scaling at an impressive growth rate and solving a hard problem that we don’t see many other companies in the space doing.”

Powered by WPeMatico

Work insights platform Fin raised $20 million in Series A funding and brought in Evan Cummack, a former Twilio executive, as its new chief executive officer.

The San Francisco-based company captures employee workflow data from across applications and turns it into productivity insights to improve the way enterprise teams work and remain engaged.

Fin was founded in 2015 by Andrew Kortina, co-founder of Venmo, and Facebook’s former VP of product and Slow Ventures partner Sam Lessin. Initially, the company was doing voice assistant technology — think Alexa but powered by humans and machine learning — and then workplace analytics software in 2020. You can read more about Fin’s origins at the link below.

The new round was led by Coatue, with participation from First Round Capital, Accel and Kleiner Perkins. The original team was talented, but small, so the new funding will build out sales, marketing and engineering teams, Cummack said.

“At that point, the right thing was to raise money, so at the end of last year, the company raised a $20 million Series A, and it was also decided to find a leadership team that knows how to build an enterprise,” Cummack told TechCrunch. “The company had completely pivoted and removed ‘Analytics’ from our name because it was not encompassing what we do.”

Fin’s software measures productivity and provides insights on ways managers can optimize processes, coach their employees and see how teams are actually using technology to get their work done. At the same time, employees are able to manage their workflow and highlight areas where there may be bottlenecks. All combined, it leads to better operations and customer experiences, Cummack said.

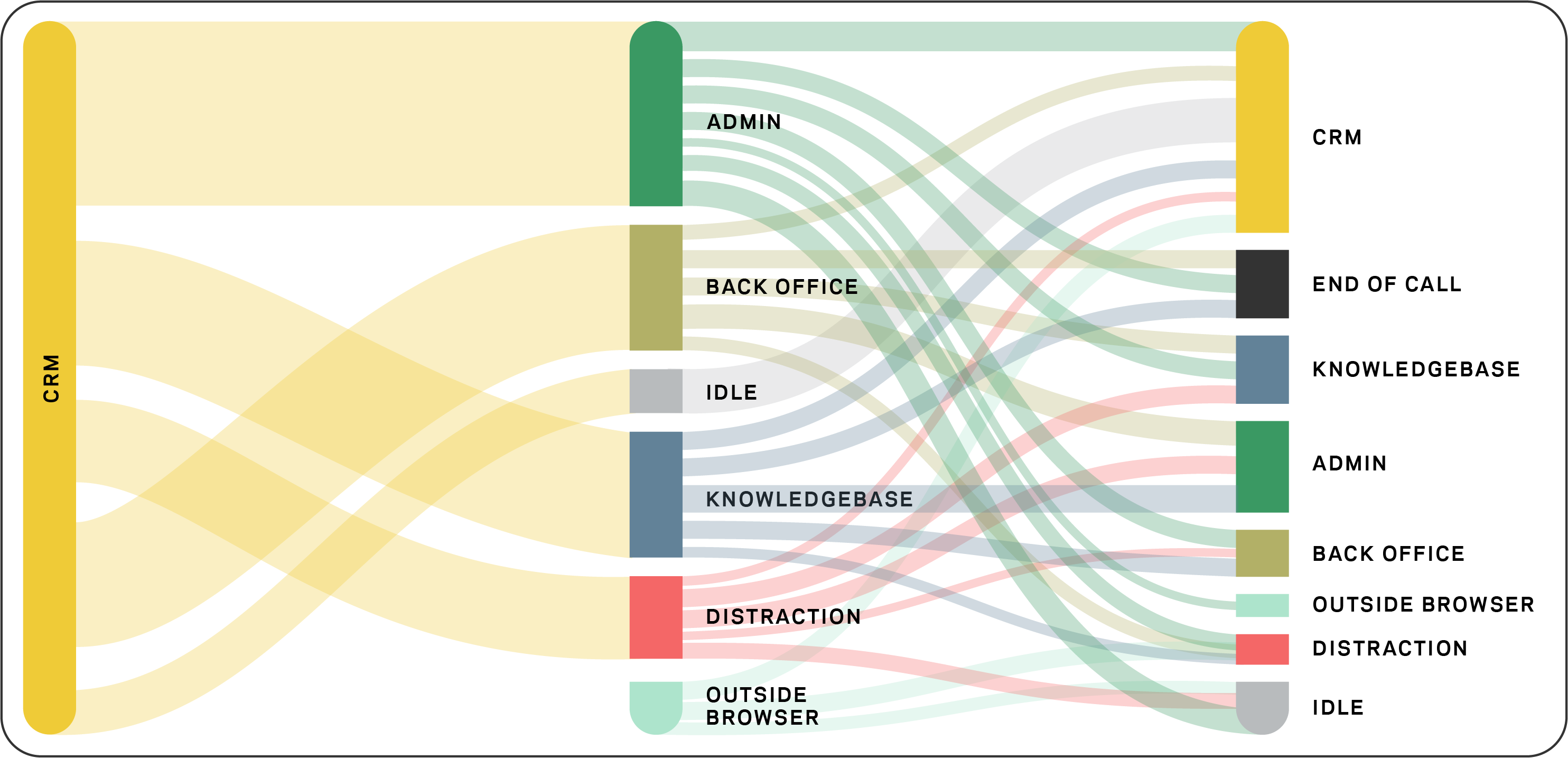

Graphic showing how work is really done. Image Credits: Fin

Fin’s view is that as more automation occurs, the company is looking at a “renaissance of human work.” There will be more jobs and more types of jobs, but people will be able to do them more effectively and the work will be more fulfilling, he added.

Particularly with the use of technology, he notes that in the era before cloud computing, there was a small number of software vendors. Now with the average tech company using over 130 SaaS apps, it allows for a lot of entrepreneurs and adoption of best-in-breed apps so that a viable company can start with a handful of people and leverage those apps to gain big customers.

“It’s different for enterprise customers, though, to understand that investment and what they are spending their money on as they use tools to get their jobs done,” Cummack added. “There is massive pressure to improve the customer experience and move quickly. Now with many people working from home, Fin enables you to look at all 130 apps as if they are one and how they are being used.”

As a result, Fin’s customers are seeing metrics like 16% increase in team utilization and engagement, a 25% decrease in support ticket handle time and a 71% increase in policy compliance. Meanwhile, the company itself is doubling and tripling its customers and revenue each year.

Now with leadership and people in place, Cummack said the company is positioned to scale, though it already had a huge head start in terms of a meaningful business.

Arielle Zuckerberg, partner at Coatue, said via email that she was part of a previous firm that invested in Fin’s seed round to build a virtual assistant. She was also a customer of Fin Assistant until it was discontinued.

When she heard the company was pivoting to enterprise, she “was excited because I thought it was a natural outgrowth of the previous business, had a lot of potential and I was already familiar with management and thought highly of them.”

She believed the “brains” of the company always revolved around understanding and measuring what assistants were doing to complete a task as a way to create opportunities for improvement or automation. The pivot to agent-facing tools made sense to Zuckerberg, but it wasn’t until the global pandemic that it clicked.

“Service teams were forced to go remote overnight, and companies had little to no visibility into what people were doing working from home,” she added. “In this remote environment, we thought that Fin’s product was incredibly well-suited to address the challenges of managing a growing remote support team, and that over time, their unique data set of how people use various apps and tools to complete tasks can help business leaders improve the future of work for their team members. We believe that contact center agents going remote was inevitable even before COVID, but COVID was a huge accelerant and created a compelling ‘why now’ moment for Fin’s solution.”

Going forward, Coatue sees Fin as “a process mining company that is focused on service teams.” By initially focusing on customer support and contact center use case — a business large enough to support a scaled, standalone business — rather than joining competitors in going after Fortune 500 companies where implementation cycles are long and there is slow time-to-value, Zuckerberg said Fin is better able to “address the unique challenges of managing a growing remote support team with a near-immediate time-to-value.”

Powered by WPeMatico

A Canadian startup called Nuula that is aiming to build a super app to provide a range of financial services to small and medium businesses has closed $120 million of funding, money that it will use to fuel the launch of its app and first product, a line of credit for its users.

The money is coming in the form of $20 million in equity from Edison Partners, and a $100 million credit facility from funds managed by the Credit Group of Ares Management Corporation.

The Nuula app has been in a limited beta since June of this year. The plan is to open it up to general availability soon, while also gradually bringing in more services, some built directly by Nuula itself but many others following an embedded finance strategy: business banking, for example, will be a service provided by a third party and integrated closely into the Nuula app to be launched early in 2022. Alongside that, the startup will also be making liberal use of APIs to bring in other white-label services, such as B2B and customer-focused payment services, starting first in the U.S. and then expanding to Canada and the U.K. before expanding further into countries across Europe.

Current products include cash flow forecasting, personal and business credit score monitoring, and customer sentiment tracking; and monitoring of other critical metrics including financial, payments and e-commerce data are all on the roadmap.

“We’re building tools to work in a complementary fashion in the app,” CEO Mark Ruddock said in an interview. “Today, businesses can project if they are likely to run out of money, and monitor their credit scores. We keep an eye on customers and what they are saying in real time. We think it’s necessary to surface for SMBs the metrics that they might have needed to get from multiple apps, all in one place.”

Nuula was originally a side-project at BFS, a company that focused on small business lending, where the company started to look at the idea of how to better leverage data to build out a wider set of services addressing the same segment of the market. BFS grew to be a substantial business in its own right (and it had raised its own money to that end, to the tune of $184 million from Edison and Honeywell). Over time, it became apparent to management that the data aspect, and this concept of a super app, would be key to how to grow the business, and so it pivoted and rebranded earlier this year, launching the beta of the app after that.

Nuula’s ambitions fall within a bigger trend in the market. Small and medium enterprises have shaped up to be a huge business opportunity in the world of fintech in the last several years. Long ignored in favor of building solutions either for the giant consumer market, or the lucrative large enterprise sector, SMBs have proven that they want and are willing to invest in better and newer technology to run their businesses, and that’s leading to a rush of startups and bigger tech companies bringing services to the market to cater to that.

Super apps are also a big area of interest in the world of fintech, although up to now a lot of what we’ve heard about in that area has been aimed at consumers — just the kind of innovation rut that Nuula is trying to get moving.

“Despite the growth in services addressing the SMB sector, overall it still lacks innovation compared to consumer or enterprise services,” Ruddock said. “We thought there was some opportunity to bring new thinking to the space. We see this as the app that SMBs will want to use everyday, because we’ll provide useful tools, insights and capital to power their businesses.”

Nuula’s priority to build the data services that connect all of this together is very much in keeping with how a lot of neobanks are also developing services and investing in what they see as their unique selling point. The theory goes like this: banking services are, at the end of the day, the same everywhere you go, and therefore commoditized, and so the more unique value-added for companies will come from innovating with more interesting algorithms and other data-based insights and analytics to give more power to their users to make the best use of what they have at their disposal.

It will not be alone in addressing that market. Others building fintech for SMBs include Selina, ANNA, Amex’s Kabbage (an early mover in using big data to help loan money to SMBs and build other financial services for them), Novo, Atom Bank, Xepelin and Liberis, biggies like Stripe, Square and PayPal, and many others.

The credit product that Nuula has built so far is a taster of how it hopes to be a useful tool for SMBs, not just another place to get money or manage it. It’s not a direct loaning service, but rather something that is closely linked to monitoring a customers’ incomings and outgoings and only prompts a credit line (which directly links into the users’ account, wherever it is) when it appears that it might be needed.

“Innovations in financial technology have largely democratized who can become the next big player in small business finance,” added Gary Golding, General Partner, Edison Partners. “By combining critical financial performance tools and insights into a single interface, Nuula represents a new class of financial services technology for small business, and we are excited by the potential of the firm.”

“We are excited to be working with Nuula as they build a unique financial services resource for small businesses and entrepreneurs,” said Jeffrey Kramer, Partner and Head of ABS in the Alternative Credit strategy of the Ares Credit Group, in a statement. “The evolution of financial technology continues to open opportunities for innovation and the emergence of new industry participants. We look forward to seeing Nuula’s experienced team of technologists, data scientists and financial service veterans bring a new generation of small business financial services solutions to market.”

Powered by WPeMatico

As companies try to navigate an ever-changing security landscape, it can be challenging to protect everything. Security startup TrueFort has built a zero trust solution focusing on protecting enterprise applications. Today, the company announced a $30 million Series B.

Shasta Ventures led today’s round with participation from new firms Canaan and Ericsson Ventures along with existing investors Evolution Equity Partners, Lytical Ventures and Emerald Development Managers. Under the terms of the agreement Nitin Chopra, managing director at Shasta Ventures, will be joining the company board. Today’s investment brings the total raised to almost $48 million.

CEO and co-founder Sameer Malhotra says that TrueFort protects customers by analyzing at each application and figuring out what normal behavior looks like. Once it understands that, it will flag anything that falls outside of the norm. The company achieves this by gathering data from partners like CrowdStrike and from multiple points within the application and infrastructure.

“Once we get this telemetry, whether it’s networks, endpoints, servers or third-party partners, we then help the customer build a picture of what those applications are doing and what’s normal behavior. We then help them baseline that, and monitor that in real time with response and real-time controls to continue those applications through their normal life cycle,” he said.

Zero trust is a concept where as a matter of policy you assume that you cannot trust any individual or device until the entity proves it belongs on your systems. Malhotra says that customers are becoming more comfortable with the concept and in 2020 the company saw massive 650% YoY revenue growth, with it up 120% YoY this year so far.

“We are seeing the demand, especially as zero trust is becoming a more familiar vernacular amongst the security community […]. Again, it’s having the visibility and understanding, and then being able to then reduce it to the limited number of acceptable relationships or executions,” he said. And he believes that it all comes down to understanding your applications and how they operate.

TrueFort co-founders Nazario Parsacala and Sameer Malhotra. Image Credits: TrueFort

The company currently has 60 employees, with hopes of reaching 85 or 90 by the end of the year. Malhotra says that as they build the employee base, they are driving to make it diverse at every level.

“We look at diversity across our whole management team, all the way from the board down to our different levels. We are quite aggressive in hiring diverse candidates, whether they’re women or LGBTQ or people of color. And we have focused programs where we work with different universities […] to bring on new employees from a diverse talent pool. We also work with different recruiters from that perspective, and our focus is always to look at a different palette and to make sure that we’re as diverse an organization as we can,” he said.

The company was founded in 2015 by Malhotra and his partner Nazario Parsacala, both of whom spent more than 20 years working at big financial services companies — Goldman Sachs and JP Morgan. They worked for a couple of years building the program, launching the first beta in 2017 before bringing the first generally available product to market the following year.

Currently customers can install the solution on prem or in the cloud of their choice, but the company has a SaaS solution in the works as well, that will be ready in the next couple of months.

Powered by WPeMatico

Organizations are swimming in data these days, and so solutions to help manage and use that data in more efficient ways will continue to see a lot of attention and business. In the latest development, SingleStore — which provides a platform to enterprises to help them integrate, monitor and query their data as a single entity, regardless of whether that data is stored in multiple repositories — is announcing another $80 million in funding, money that it will be using to continue investing in its platform, hiring more talent and overall business expansion. Sources close to the company tell us that the company’s valuation has grown to $940 million.

The round, a Series F, is being led by Insight Partners, with new investor Hewlett Packard Enterprise, and previous backers Khosla Ventures, Dell Technologies Capital, Rev IV, Glynn Capital and GV (formerly Google Ventures) also participating. The startup has to date raised $264 million, including most recently an $80 million Series E last December, just on the heels of rebranding from MemSQL.

The fact that there are three major strategic investors in this Series F — HPE, Dell and Google — may say something about the traction that SingleStore is seeing, but so too do its numbers: 300%+ increase in new customer acquisition for its cloud service and 150%+ year-over-year growth in cloud.

Raj Verma, SingleStore’s CEO, said in an interview that its cloud revenues have grown by 150% year over year and now account for some 40% of all revenues (up from 10% a year ago). New customer numbers, meanwhile, have grown by over 300%.

“The flywheel is now turning around,” Verma said. “We didn’t need this money. We’ve barely touched our Series E. But I think there has been a general sentiment among our board and management that we are now ready for the prime time. We think SingleStore is one of the best-kept secrets in the database market. Now we want to aggressively be an option for people looking for a platform for intensive data applications or if they want to consolidate databases to one from three, five or seven repositories. We are where the world is going: real-time insights.”

With database management and the need for more efficient and cost-effective tools to manage that becoming an ever-growing priority — one that definitely got a fillip in the last 18 months with COVID-19 pushing people into more remote working environments. That means SingleStore is not without competitors, with others in the same space, including Amazon, Microsoft, Snowflake, PostgreSQL, MySQL, Redis and more. Others like Firebolt are tackling the challenges of handing large, disparate data repositories from another angle. (Some of these, I should point out, are also partners: SingleStore works with data stored on AWS, Microsoft Azure, Google Cloud Platform and Red Hat, and Verma describes those who do compute work as “not database companies; they are using their database capabilities for consumption for cloud compute.”)

But the company has carved a place for itself with enterprises and has thousands now on its books, including GE, IEX Cloud, Go Guardian, Palo Alto Networks, EOG Resources and SiriusXM + Pandora.

“SingleStore’s first-of-a-kind cloud database is unmatched in speed, scale, and simplicity by anything in the market,” said Lonne Jaffe, managing director at Insight Partners, in a statement. “SingleStore’s differentiated technology allows customers to unify real-time transactions and analytics in a single database.” Vinod Khosla from Khosla Ventures added that “SingleStore is able to reduce data sprawl, run anywhere, and run faster with a single database, replacing legacy databases with the modern cloud.”

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

Meetings are an inevitable part of the work day, but as workplaces became more distributed over the past 18 months, Vowel CEO Andy Berman says we are steadily moving toward “death by meeting.”

His virtual meeting platform is the latest to receive venture capital funding — $13.5 million — with the goal of making meetings more useful before, during and after.

Vowel is launching a meeting operating system with tools like real-time transcription; integrated agendas, notes and action items; meeting analytics; and searchable, on-demand recordings of meetings. The company has a freemium business model and will also be rolling out a business plan this fall for $16 per user per month. Extra features will include advanced integrations, security and admin controls.

The Series A was led by David Hornik of Lobby Capital, who was joined by existing investors Amity Ventures and Box Group and a group of individual investors, including Calendly CEO Tope Awotona, Intercom co-founder Des Traynor, Slack VP Ethan Eismann, former Yammer executive Viviana Faga, former InVision president David Fraga and Okta co-founder Frederic Kerrest.

Prior to starting Vowel, Berman was one of the founders of baby monitor company Nanit. The company had teams spread out around the world, and communication was tough as a result. In 2018, the company went looking for a tool that would work for synchronous and asynchronous meetings, but there were still a lot of time zones to manage, he said.

Taking a cue from Nanit’s own baby monitors that were streaming video over 17 hours a day, the idea for Vowel was born, and the company began to focus on the hypothesis that distributed work would be prevalent.

“People initially thought we were crazy, but then the pandemic hit, and everyone was learning how to work remotely,” Berman told TechCrunch. “As we now go back to hybrid work, we see this as an opportunity.”

In 2017, Harvard Business Review reported that executives spent 23 hours in meetings each week. Berman now estimates that the average worker spends half of their time each week in meetings.

Vowel is out to bring Slack, Figma and GitHub components to meetings by recording audio and video that can be paused at any time. Users can add notes and see where those notes fall within a real-time transcription that enables people who arrive late or could not make the meeting to catch up easily. After meetings are over, they can be shared, and Vowel has a search function so that users can go back and see where a particular person or topic was discussed.

The new funding will enable the company to grow its team in product, design and engineering. Vowel plans to hire up to 30 new people over the next year. The company recently closed its beta test and has amassed a 10,000-person waitlist. The public launch will happen in the fall, Berman said.

Workplace productivity and office communication tools are not new concepts, but as Berman explained, became increasingly important when homes became offices over the past 18 months.

Competitors took different approaches to solving these problems: focusing on video conferencing or audio or meeting management with plugins. Berman says an area where many have not succeeded yet is integrating meetings into the typical workflow. That’s where Vowel comes in with its “meeting OS,” he added.

“Our goal is to make meetings more inclusive and worthwhile, which includes the prep, the meeting and the follow-up,” Berman said. “We see the future will be about knowledge management, so the difference between what we are doing is ensuring you can catch up quickly and keep that knowledge base. A Garner report said that 75% of workplace meetings will be recorded by 2025, and that is a trend we are reinventing from the ground up.”

David Hornik, founding partner at Lobby Capital, said he became acquainted with Vowel from its existing investor Amity Ventures. Hornik, who sits on the GitLab board, said GitLab was one of the largest distributed companies in the tech space, prior to the pandemic, and saw first-hand the challenge of making distributed teams functionable.

When Hornik heard about Vowel, he said he “jumped quickly” on the opportunity. His firm typically invests in platform businesses that have the capacity to transform business spaces. Many are pure software, like Splunk or GitLab, while others are akin to Bill.com, which transformed how small businesses manage financial operations, he added.

All of those combine into a company, like Vowel, especially given the company’s vision for a meeting OS to transform a meeting space that hadn’t moved forward in decades, he said.

“This was quickly obvious to me because my day is meetings — an eight-Zoom day is a normal day — I just wish I could remember everything,” Hornik said. “Speaking with early customers using the product, when I asked them what they would do if this ever went away, the first thing they said was ‘cry,’ and, because there was no alternative, would return to Zoom or other tools, but it would be a big setback.”

Powered by WPeMatico