Fundings & Exits

Auto Added by WPeMatico

Auto Added by WPeMatico

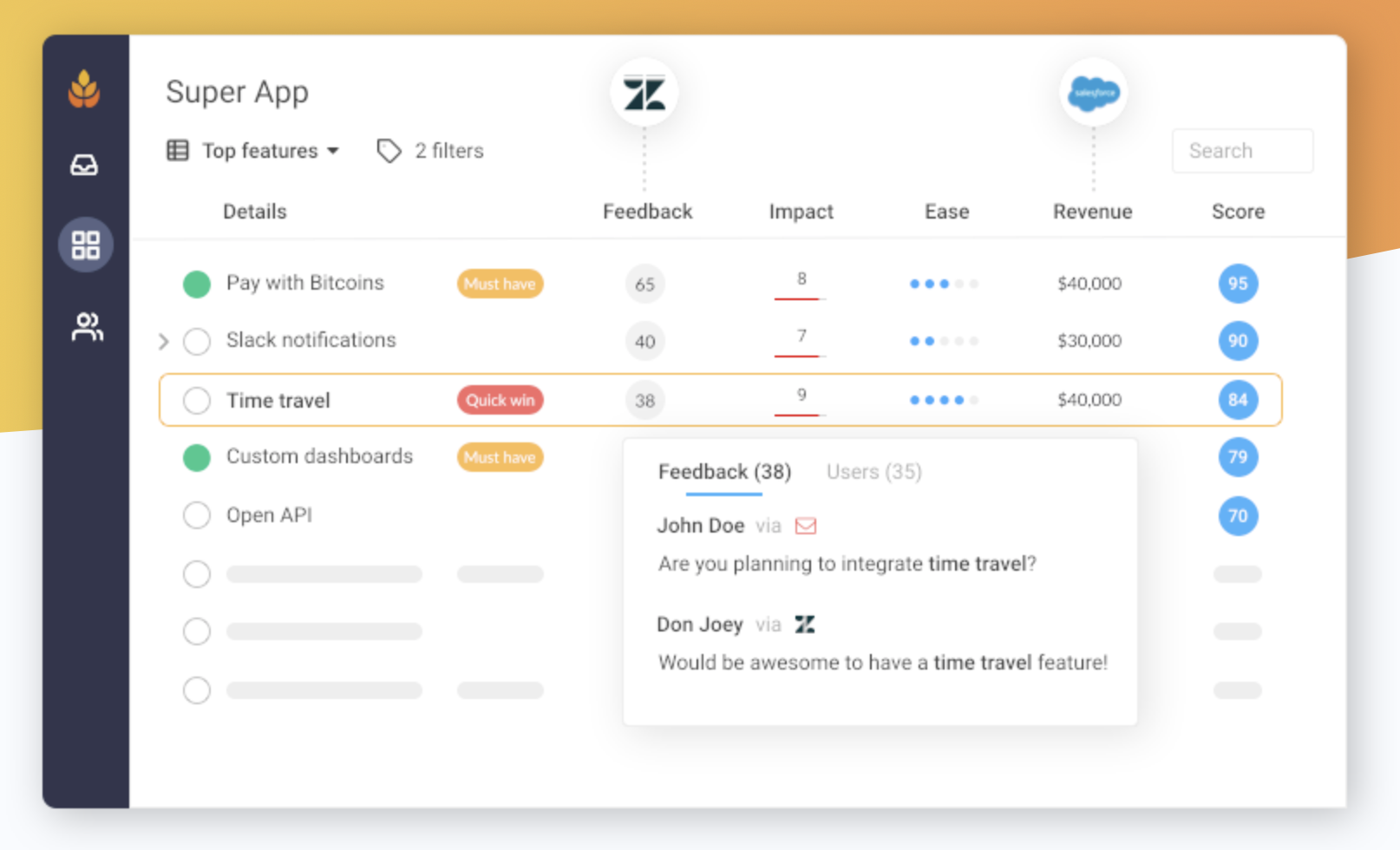

Meet Harvestr, a software-as-a-service startup that wants to help product managers centralize customer feedback from various places. Product managers can then prioritize outstanding issues and feature requests. Finally, the platform helps you get back to your customers once changes have been implemented.

The company just raised a $650,000 funding round led by Bpifrance, with various business angels also participating, such as 360Learning co-founders Nicolas Hernandez and Guillaume Alary, as well as Station F director Roxanne Varza through the Atomico Angel Programme.

Harvestr integrates directly with Zendesk, Intercom, Salesforce, Freshdesk, Slack and Zapier. For instance, if a user opens a ticket on Zendesk and another user interacts with your support team through an Intercom chat widget, everything ends up in Harvestr.

Once you have everything in the system, Harvestr helps you prioritize tasks that seem more urgent or that are going to have a bigger impact.

When you start working on a feature or when you’re about to ship it, you can contact your users who originally reached out to talk to you about it.

Eventually, Harvestr should help you build a strong community of power users around your product. And there are many advantages in pursuing this strategy.

First, you reward your users by keeping them in the loop. It should lead to higher customer satisfaction and lower churn. Your most engaged customers could also become your best ambassadors to spread the word around.

Harvestr costs $49 per month for five seats and $99 per month for 20 seats. People working for 360Learning, HomeExchange, Dailymotion and other companies are currently using it.

Powered by WPeMatico

When Visa bought Plaid this week for $5.3 billion, a figure that was twice its private valuation, it was a clear signal that traditional financial services companies are looking for ways to modernize their approach to business.

With Plaid, Visa picks up a modern set of developer APIs that work behind the scenes to facilitate the movement of money. Those APIs should help Visa create more streamlined experiences (both at home and inside other companies’ offerings), build on its existing strengths and allow it to do more than it could have before, alone.

But don’t take our word for it. To get under the hood of the Visa-Plaid deal and understand it from a number of perspectives, TechCrunch got in touch with analysts focused on the space and investors who had put money into the erstwhile startup.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re continuing our exploration of companies that have reached material scale, usually viewed through the lens of annual recurring revenue (ARR). We’ve looked at companies that have reached the $100 million ARR mark and a few that haven’t quite yet, but are on the way.

Today, a special entry. We’re looking at a company that isn’t yet at the $100 million ARR mark. It’s 60% of the way there, but with a twist. The company is bootstrapped. Yep, from pre-life as a consultancy that built a product to fit its own needs, Cloudinary is cruising toward nine-figure recurring revenue and an IPO under its own steam.

Powered by WPeMatico

French startup Lydia is raising a $45 million Series B round (€40 million). Tencent is leading the round with existing investors CNP Assurances, XAnge and New Alpha also participating.

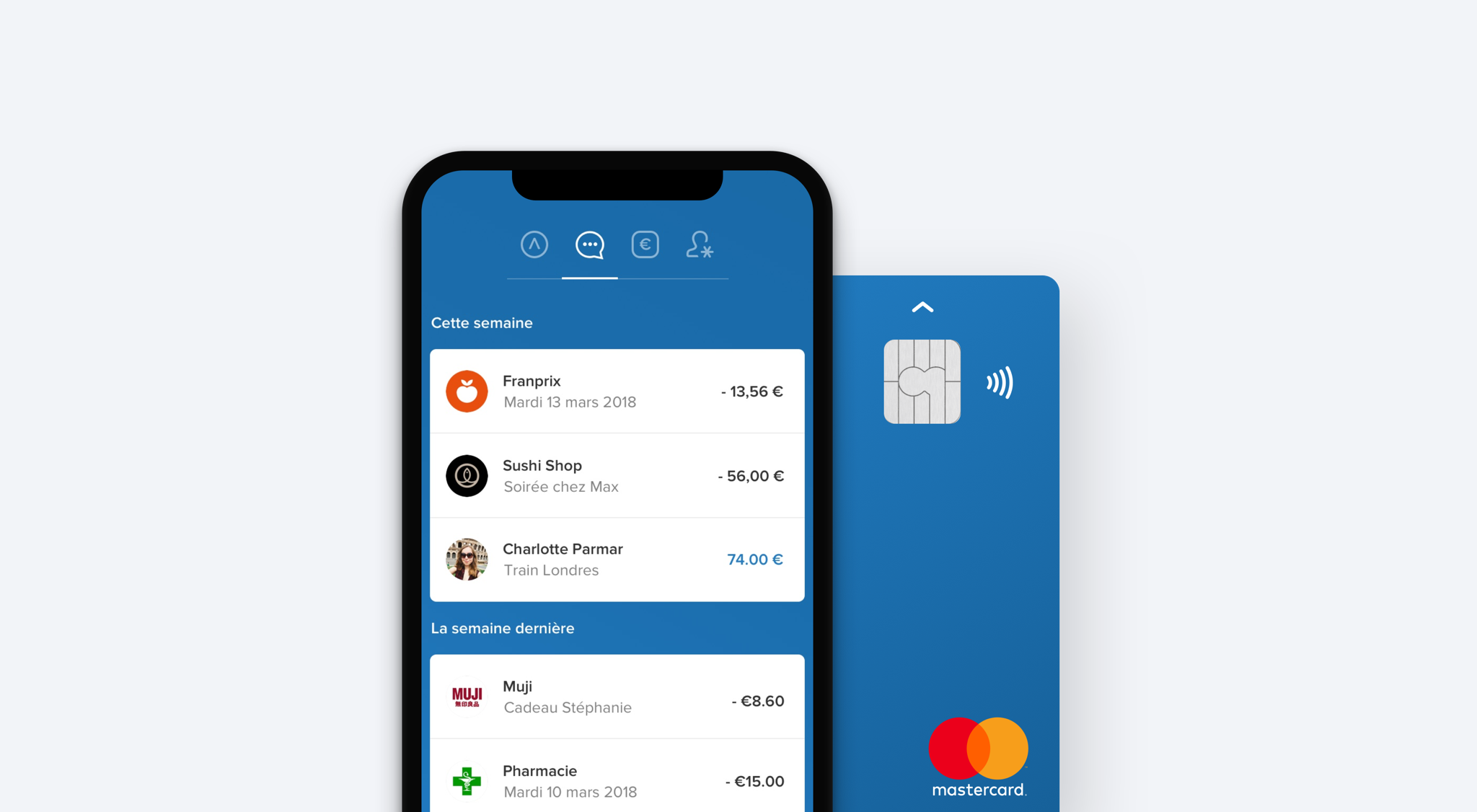

If you live in France, chances are you already know Lydia quite well. The company has become a ubiquitous mobile payment app, especially for people under 30 years old. Think about it as a sort of Square Cash or Venmo, but for France.

“At first, we wanted to raise less but we ended up raising more,” Lydia co-founder and CEO Cyril Chiche told me in a phone interview.

The company has managed to attract 3 million users in France. More impressive, 25% of French people between 18 and 30 years old have a Lydia account — and 5,000 people sign up every day. Lydia currently has 90 employees.

More recently, the company has expanded beyond peer-to-peer payment. First, the company wants to help you manage your money in many different ways with an important value — everything should happen in real time.

You can create multiple Lydia accounts to put some money aside or use money in that sub-account for a specific purpose. That feature alone turns the app into a versatile money management app.

For instance, you can associate a Lydia payment card with a Lydia account and a virtual card with another Lydia account — that virtual card works with Apple Pay, Google Pay, Samsung Pay and more. You can change those settings in real time.

You can share accounts with other Lydia users. And shared accounts are truly shared — everyone can top up and withdraw money from that account. You can spend directly from that account or withdraw money to another account.

You can also turn any Lydia account into a money pot account. In just a few taps, you can generate a link and share it with your friends so that they can add money using their regular payment card or a Lydia account.

More recently, the company has introduced “the market”, a marketplace of other financial products. From the Lydia app, you can borrow up to €1,000 in just a few seconds. You can also insure your phone and other mobile devices. You can get some free credit when you open a bank account, insure your home with Luko, switch to another electricity and gas provider, compare mobile phone and internet providers and more.

And that strategy is going to be key in the future. “We have an ambitious goal, which is turning Lydia into a mobile financial service app,” Chiche said.

He also pointed out that the company that has been the most successful when it comes to creating a mobile marketplace of financial products is Tencent with WeChat.

“Tencent is also the number one player in the video game industry, and there’s no industry with as much user engagement,” Chiche said. Tencent acquired Supercell, bought 40% of Epic Games, acquired Riot Games (League of Legends), invested in Ubisoft, Activision Blizzard, Discord, etc. Lydia hopes that it can learn from Tencent on the user engagement front.

Compared to many fintech startups, Lydia doesn’t want to replace banks altogether — the company says it wants to build a meta-banking app. Peer-to-peer payments represent the top of the funnel and a great user acquisition strategy thanks to networking effects.

You can then connect your Lydia account with your bank account and your debit card. This way, you can send money back and forth between your Lydia accounts and your bank account. As a user, that strategy slowly pays off over time. After a while, you end up spending money directly from your Lydia account and relying more heavily on Lydia’s native payment features, with your bank account acting as a money back end.

At the bottom of the funnel, Lydia hopes that it can turn active Lydia users into paid customers with a handful of in-house and third-party financial products. In other words, Lydia doesn’t want to become a credit institution like a traditional bank, it wants to become a financial hub. Expanding the marketplace will be a big focus for the company going forward.

While Lydia is available in other European countries, Lydia is still massively used in its home market with other markets lagging behind. With today’s funding round, growth in foreign countries is going to be the second key topic.

Powered by WPeMatico

ActionIQ co-founder and CEO Tasso Argyros knows there are plenty of companies promising to help businesses use their customer data to deliver personalized experiences — as he put it, “The space has gotten very, very hot over the last couple of years.”

But in the face of growing competition, ActionIQ (founded in 2014 and headquartered in New York) has attracted some impressive customers, like The New York Times, Conde Nast, American Eagle Outfitters, Vera Bradley and Pandora Media, as well as high-profile investors like Sequoia Capital and Andreessen Horowitz.

Today, it’s announcing that it has raised $32 million in Series C funding.

“At this point, we believe we are four to five years ahead of the market,” Argyros told me. “[Customer data platforms are] very hot, you see people really jumping into it, but nobody really has a product.”

He attributed the rise of these platforms to the growth in customer acquisition costs: “Everybody’s switched their focus from ‘How do we acquire more customers?’ to ‘How do you grow lifetime value?’ ”

The key, Argyros said, is “delivering personalized experiences at scale.” So if you’re a business trying to understand which customers need to be convinced to stick around, which customers are ready to upgrade to a paid subscription and so on, you need a platform like ActionIQ: “What’s common about all these questions is that they’re all data questions.”

He described ActionIQ’s approach as “product-first,” creating self-serve tools for enterprises rather than relying on consulting or IT services, and he said the product is designed to “drive intelligent actions activated through any channel.”

Argyros contrasted this approach with the large marketing clouds, where he said that stitching together products from various acquisitions has led to “a huge data gap between what marketing clouds promise and what they can actually deliver.” And he said other customer data platforms are limited to bringing the data together — but “just putting customer data in one place, that doesn’t mean business can use the customer data to drive value.”

March Capital Partners led the round, with participation from Cisco Ventures, as well as previous investors Sequoia, Andreessen and FirstMark Capital. Meredith Finn, a partner at March, is joining ActionIQ’s board of directors.

“From my professional experience at Salesforce and Twitter, when it comes to building a relationship with your customers, data is everything,” Finn said in a statement. “ActionIQ took a data-first approach from day one in contrast to many vendors that are now scrambling to address their data gaps by duct-taping data infrastructure to their existing point solutions. … The potential of such a platform is limitless, and spans well beyond traditional marketing channels to other areas of customer interactions including web and mobile app experiences, customer support and sales.”

ActionIQ has now raised a total of $75 million in funding. And while the Series C isn’t significantly larger that the $30 million that ActionIQ raised in 2017, Argyros said the company didn’t need to raise a huge round this time around, because it’s already built out the core product.

“A lot of dollars were invested heavily in the product way before the demand was there,” he said. “The Series B was pretty significant because there was so much upfront product investment. … Most of these funds are going towards expanding the business in sales and marketing.”

Powered by WPeMatico

Not the city, the $57 million-funded cryptocurrency custodian startup. When someone wants to keep safe tens or hundreds of millions of dollars in Bitcoin, Ethereum or other coins, they put them in Anchorage’s vault. And now they can trade straight from custody so they never have to worry about getting robbed mid-transaction.

With backing from Visa, Andreessen Horowitz and Blockchain Capital, Anchorage has emerged as the darling of the cryptocurrency security startup scene. Today it’s flexing its muscle and war chest by announcing its first acquisition, crypto risk modeling company Merkle Data.

Anchorage Founders

Anchorage has already integrated Merkle’s technology and team to power today’s launch of its new trading feature. It eliminates the need for big crypto owners to manually move assets in and out of custody to buy or sell, or to set up their own in-house trading. Instead of grabbing some undisclosed spread between the spot price and the price Anchorage quotes its clients, it charges a transparent per transaction fee of a tenth of a percent.

It’s stressful enough trading around digital fortunes. Anchorage gives institutions and token moguls peace of mind throughout the process while letting them stake and vote while their riches are in custody. Anchorage CEO Nathan McCauley tells me, “Our clients want to be able to fund a bank account with USD and have it seamlessly converted into crypto, securely held in their custody accounts. Shockingly, that’s not yet the norm — but we’re changing that.”

Founded in 2017 by leaders behind Docker and Square, Anchorage’s core business is its omnimetric security system that takes out of the equation passwords that can be lost or stolen. Instead, it uses humans and AI to review scans of your biometrics, nearby networks and other data for identity confirmation. Then it requires consensus approval for transactions from a set of trusted managers you’ve whitelisted.

With Anchorage Trading, the startup promises efficient order routing, transparent pricing and multi-venue liquidity from OTC desks, exchanges and market makers. “Because trading and custody are directly integrated, we’re able to buy and sell crypto from custody, without having to make risky external transfers or deal with multiple accounts from different providers,” says Bart Stephens, founder and managing partner of Blockchain Capital.

Trading isn’t Anchorage’s primary business, so it doesn’t have to squeeze clients on their transactions, and can instead try to keep them happy for the long-term. That also sets up Anchorage to be a foundational part of the cryptocurrency stack. It wouldn’t disclose the terms of the Merkle Data acquisition, but the Pantera Capital-backed company brings quantitative analysts to Anchorage to keep its trading safe and smart.

“Unlike most traditional financial assets, crypto assets are bearer assets: In order to do anything with them, you need to hold the underlying private keys. This means crypto custodians like Anchorage must play a much larger role than custodians do in traditional finance,” says McCauley. “Services like trading, settlement, posting collateral, lending and all other financial activities surrounding the assets rely on the custodian’s involvement, and in our view are best performed by the custodian directly.”

Anchorage will be competing with Coinbase, which offers integrated custody and institutional brokerage through its agency-only OTC desk. Fidelity Digital Assets combines trading and brokerage, but for Bitcoin only. BitGo offers brokerage from custody through a partnership with Genesis Global Trading. But Anchorage hopes its experience handling huge sums, clear pricing and credentials like membership in Facebook’s Libra Association will win it clients.

McCauley says the biggest threat to Anchorage isn’t competitors, though, but hazy regulation. Anchorage is building a core piece of the blockchain economy’s infrastructure. But for the biggest financial institutions to be comfortable getting involved, lawmakers need to make it clear what’s legal.

Powered by WPeMatico

Google announced today that it is buying AppSheet, an eight-year-old no-code mobile-application-building platform. The company had raised more than $17 million on a $60 million valuation, according to PitchBook data. The companies did not share the purchase price.

With AppSheet, Google gets a simple way for companies to build mobile apps without having to write a line of code. It works by pulling data from a spreadsheet, database or form, and using the field or column names as the basis for building an app.

It is integrated with Google Cloud already integrating with Google Sheets and Google Forms, but also works with other tools, including AWS DynamoDB, Salesforce, Office 365, Box and others. Google says it will continue to support these other platforms, even after the deal closes.

As Amit Zavery wrote in a blog post announcing the acquisition, it’s about giving everyone a chance to build mobile applications, even companies lacking traditional developer resources to build a mobile presence. “This acquisition helps enterprises empower millions of citizen developers to more easily create and extend applications without the need for professional coding skills,” he wrote.

In a story we hear repeatedly from startup founders, Praveen Seshadri, co-founder and CEO at AppSheet, sees an opportunity to expand his platform and market reach under Google in ways he couldn’t as an independent company.

“There is great potential to leverage and integrate more deeply with many of Google’s amazing assets like G Suite and Android to improve the functionality, scale, and performance of AppSheet. Moving forward, we expect to combine AppSheet’s core strengths with Google Cloud’s deep industry expertise in verticals like financial services, retail, and media and entertainment,” he wrote.

Google sees this acquisition as extending its development philosophy with no-code working alongside workflow automation, application integration and API management.

No code tools like AppSheet are not going to replace sophisticated development environments, but they will give companies that might not otherwise have a mobile app the ability to put something decent out there.

Powered by WPeMatico

Equinix announced today that it is acquiring bare metal cloud provider Packet, the New York City startup that had raised over $36 million on a $100 million valuation, according to PitchBook data.

Equinix has a set of data centers and co-location facilities around the world. Companies that may want to have more control over their hardware could use their services, including space, power and cooling systems, instead of running their own data centers.

Equinix is getting a unique cloud infrastructure vendor in Packet, one that can provide more customized kinds of hardware configurations than you can get from the mainstream infrastructure vendors like AWS and Azure. Company COO George Karidis described what separated his company from the pack in a September, 2018 TechCrunch article:

“We offer the most diverse hardware options,” he said. That means they could get servers equipped with Intel, ARM, AMD or with specific nVidia GPUs in whatever configurations they want. By contrast public cloud providers tend to offer a more off-the-shelf approach. It’s cheap and abundant, but you have to take what they offer, and that doesn’t always work for every customer.

In a blog post announcing the deal, company co-founder and CEO Zachary Smith had a message for his customers, who may be worried about the change in ownership. “When the transaction closes later this quarter, Packet will continue operating as before: same team, same platform, same vision,” he wrote.

He also offered the standard value story for a deal like this, saying the company could scale much faster under Equinix than it could on its own, with access to its new company’s massive resources, including 200+ data centers in 55 markets and 1,800 networks.

Sara Baack, chief product officer at Equinix, says bringing the two companies together will provide a diverse set of bare metal options for customers moving forward. “Our combined strengths will further empower companies to be everywhere they need to be, to interconnect everyone and integrate everything that matters to their business,” she said in a statement.

While the companies did not share the purchase price, they did hint that they would have more details on the transaction after it closes, which is expected in the first quarter this year.

Powered by WPeMatico

Seventy-five-million-dollar-funded legal services startup Atrium doesn’t want to be the next company to implode as the tech industry tightens its belt and businesses chase margins instead of growth via unsustainable economics. That’s why Atrium is laying off most of its in-house lawyers.

Now, Atrium will focus on its software for startups navigating fundraising, hiring and collaborating with lawyers. Atrium plans to ramp up its startup advising services. And it’s also doubling down on its year-old network of professional service providers that help clients navigate day-to-day legal work. Atrium’s laid-off attorneys will be offered spots as preferred providers in that network if they start their own firm or join another.

“It’s a natural evolution for us to create a sustainable model,” Atrium co-founder and CEO Justin Kan tells TechCrunch. “We’ve made the tough decision to restructure the company to accommodate growth into new business services through our existing professional services network,” Kan wrote on Atrium’s blog. He wouldn’t give exact figures, but confirmed that more than 10 but less than 50 staffers are impacted by the change, with Atrium having a headcount of 150 as of June.

The change could make Atrium more efficient by keeping fewer expensive lawyers on staff. However, it could weaken its $500 per month Atrium membership that included some services from its in-house lawyers that might be more complicated for clients to get through its professional network. Atrium will also now have to prove the its client-lawyer collaboration software can survive in the market with firms paying for it rather than it being bundled with its in-house lawyers’ services.

“We’re making these changes to move Atrium to a sustainable model that provides high-quality services to our clients. We’re doing it proactively because we see the writing on the wall that it’s important to have a sustainable business,” Kan says. “That’s what we’re doing now. We don’t anticipate any disruption of services to clients. We’re still here.”

Justin Kan (Atrium) at TechCrunch Disrupt SF 2017

Founded in 2017, Atrium promised to merge software with human lawyers to provide quicker and cheaper legal services. Its technology can help automatically generate fundraising contracts, hiring offers and cap tables for startups while using machine learning to recommend procedures and clauses based on anonymized data from its clients. It also serves like a Dropbox for legal, organizing all of a startup’s documents to ensure everything’s properly signed and teams are working off the latest versions without digging through email.

The $500 per month Atrium membership offered this technology plus limited access to an in-house startup lawyer for consultation, plus access to guide books and events. Clients could pay extra if they needed special help such as with finalizing an acquisition deal, or access to its Fundraising Concierge service for aid with developing a pitch and lining up investor meetings.

Kan tells me Atrium still has some in-house lawyers on staff, which will help it honor all its existing membership contracts and power its new emphasis on advising services. He wouldn’t say if Atrium is paid any equity for advising, or just cash. The membership plan may change for future clients, so lawyer services are provided through its professional network instead.

“What we noticed was that Atrium has done a really good job of building a brand with startups. Often what they wanted from attorneys was…advice on ‘how to set my company up,’ ‘how to set my sales and marketing team up,’ ‘how to get great terms in my fundraising process,’ ” so Atrium is pursuing advising, Kan tells me. “As we sat down to look at what’s working and what’s not working, our focus has been to help founders with their super-hero story, connect them with the right providers and advisors, and then helping quarterback everything you need with our in-house specialists.”

LawSites first reported Saturday that Atrium was laying off in-house lawyers. A source says that Atrium’s lawyers only found out a week ago about the changes, and they’ve been trying to pitch Atrium clients on working with them when they leave. One Atrium client said they weren’t surprised by the changes because they got so much legal advice for just $500 per month, which they suspected meant Atrium was losing money on the lawyers’ time as it was so much less expensive than competitors. They also said these cheap legal services rather than the software platform were the main draw of Atrium, and they’re unsure if the tech on its own is valuable enough.

One concern is Atrium might not learn as quickly about which services to translate into software if it doesn’t have as many lawyers in-house. But Kan believes third-party lawyers might be more clear and direct about what they need from legal technology. “I feel like having a true market for the software you’re building is better than having an internal market,” he says. “We get feedback from the outside firms we work with. I think in some ways that’s the most valuable feedback. I think there’s a lot of false signals that can happen when you’re the both the employer and the supplier.”

It was critical for Atrium to correct course before getting any bigger, given the fundraising problems hitting late-stage startups with poor economics in the wake of the WeWork debacle and SoftBank’s troubles. Atrium had raised a $10.5 million Series A in 2017 led by General Catalyst alongside Kleiner, Founders Fund, Initialized and Kindred Ventures. Then in September 2018, it scored a huge $65 million Series B led by Andreessen Horowitz.

Raising even bigger rounds might have been impossible if Atrium was offering consultations with lawyers at far below market rate. Now it might be in a better position to attract funding. But the question is whether clients will stick with Atrium if they get less access to a lawyer for the same price, and whether the collaboration platform is useful enough for outside law firms to pay for.

Kan had gone through tough pivots in the past. He had strapped a camera to his head to create content for his live-streaming startup Justin.tv, but wisely recentered on the 3% of users letting people watch them play video games. Justin.tv became Twitch and eventually sold to Amazon for $970 million. His on-demand personal assistant startup Exec had to switch to just cleaning in 2013 before shutting down due to rotten economics.

Rather than deny the inevitable and wait until the last minute, with Atrium Kan tried to make the hard decision early.

Powered by WPeMatico

E-commerce phenom and D2C bright light Casper has filed to go public.

The New York-based company that raised nearly $340 million while private, according to Crunchbase data, expects to trade on the New York Stock Exchange under the ticker symbol “CSPR.” Its S-1 filing includes a $100 million placeholder figure for its possible capital raise.

The company will need the money, as it loses money and burns cash. Let’s explore just how a mattress company does that.

In the full years of 2017 and 2018, Casper recorded revenue of $250.9 million (net of $45.7 million in “refunds, returns, and discounts”) and $357.9 million (net of $80.7 million in “refunds, returns, and discounts”). That worked out to growth of 42.6% in the year.

Over the same two periods, Casper lost $73.4 million and $92.1 million on a net basis, respectively.

In the first three quarters of 2019 versus 2018, Casper put up $312.3 million in top line (net of $80.1 million in “refunds, returns, and discounts”), up just over 20% from its year-ago three-quarter tally of $259.7 million in revenue (net of $57.7 million in “refunds, returns, and discounts”).

The company’s net loss during the three-quarter period rose from $64.2 million in 2018 to $67.4 million in 2019. The company’s net losses are generally rising (though slowly so far in 2019), while its growth decelerates.

In contrast, and to the company’s favor, its operating cash burn is slowing. From $84.0 million in 2017 to $72.3 million in calendar 2018, Casper slowed its operating cash consumption further in 2019, to just $29.7 million in the first three quarters of the year, compared to $44.9 million over the same period of the preceding year.

But the company’s slowing growth and stiff losses using regular accounting methods (GAAP) could strain its valuation. Casper was valued at $1.1 billion in its most recent funding round.

While the company’s gross margins aren’t bad for a non-software company (49.6% in the first nine months of 2019), the firm spent over 73% of its gross profit last year on sales and marketing costs. That figure indicates that Casper spent heavily to generate growth, growth that came in at about 20% so far in 2019, as reported.

That fact implies that growth will remain constrained, as the firm can’t afford to spend too much more on the line item. Which begs the question: What’s the value of a firm that is showing slowing growth, non-recurring revenue and sticky GAAP losses?

The company’s adjusted losses aren’t much better. Looking at its adjusted EBITDA, a profit metric so distorted to flatter that it’s nigh a funhouse mirror, Casper only marginally improved on its 2018 tally looking at the first three quarters of that year (-$57.5 million) in 2019 (-$53.8 million).

Casper has raised from IVP, Lerer Hippeau, Target and New Enterprise Associates. The firm raised seed capital back in 2014 along with a Series A. Lerer and NEA were most active back then, looking at its funding history.

The company raised $55 million more in 2015, and a far-larger $170 million in mid-2017. A $100 million round came in 2019 that set it up for its 2020 IPO.

This company’s IPO is a pricing question. And one that will impact a host of startups that both compete directly with Casper or operate in a different vertical with a similar business. Get hype.

Powered by WPeMatico