TC

Auto Added by WPeMatico

Auto Added by WPeMatico

The wave of venture capital interest in geographies other than Silicon Valley has been building momentum over the past 5+ years. If you measure capital flow by Twitter chatter alone, you may assume the tidal wave is about to break and checks are being doled out via T-shirt launchers repurposed from hockey games.

Meanwhile, VCs will approach founders saying, “We are now looking into markets beyond Silicon Valley.”

When Mucker launched back in 2011, our founding partners, who had left Silicon Valley for LA, set out to prove that high-growth companies can be built anywhere. Our portfolio from this past decade is a testament to this very narrative. With offices in LA, Austin and Nashville — and investments all over North America, we are seeing a marked increase in receptivity to an idea we had over a decade ago to invest across the U.S. and into Canada.

As of late, I’m receiving more and more outreach from VCs based in San Francisco, New York and beyond interested in deal flow here in Nashville and the Southeast.

When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

In reality, there will be some lag time before the checks being written by these same VCs are consistent with both the outward hype and existing market opportunity. The broadened geographic focus of VCs for marketing purposes and FOMO is not adequately capturing the real narrative.

In short: When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

“We” is a loaded declaration. I write this as a venture capitalist and also as the biracial daughter of a first-generation immigrant, with both of my parents growing up poor by most people’s standards. One branch of my family immigrated to the U.S. from Mexico during the Mexican Revolution, the other harkens back to rural Oklahoma. The founders I meet day in and day out in the Southeast oftentimes tell a similar story.

My story is that of the average American, and yet feels light years apart from what people perceive as the “innovation economy.” Many of the people I’ve met in venture capital this past decade come from prestigious lineages with parents and grandparents who may have never associated with mine. And yet, here we are. This is America.

While Silicon Valley’s origins and climb to international stardom center around a collection of innovators, attracting more innovators and capital as the decades passed, one critical element arguably fell by the wayside — America as an expansive and diverse collection of states and people. Annual reporting on where venture capital dollars flow supports this discrepancy, with the majority of funds being funneled into companies based in and around Silicon Valley.

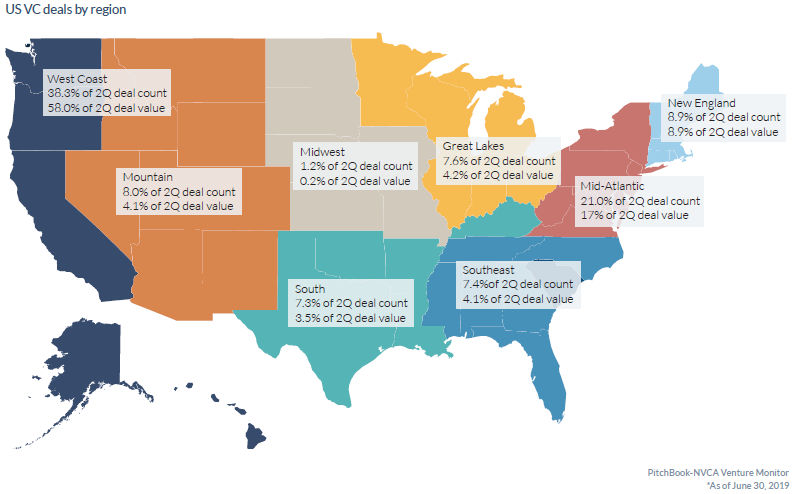

U.S. VC deals by region, as of June 2019. Image Credits: PitchBook/NVCA Venture Monitor

We find ourselves at the threshold of a decade where America will be rightfully recast as the land of opportunity for VC dollars to flow into the products and services fueling America’s future. And, at the helm of such innovations needs to be the people closest to these market opportunities, in full alignment with their customers and the nuances to best serve them.

In a post-COVID world, customers have never demanded more transparency into supply chains, workplace culture and equity ownership. Customers are more informed than ever before, with a 24/7 info line on brands and a growing scrutiny on where to place their hard-earned dollars. In short, they demand to be seen, and the founders who recognize this are the ones thriving in this new climate.

Where do the customers live? I’ll give you a hint: They are largely not in Silicon Valley.

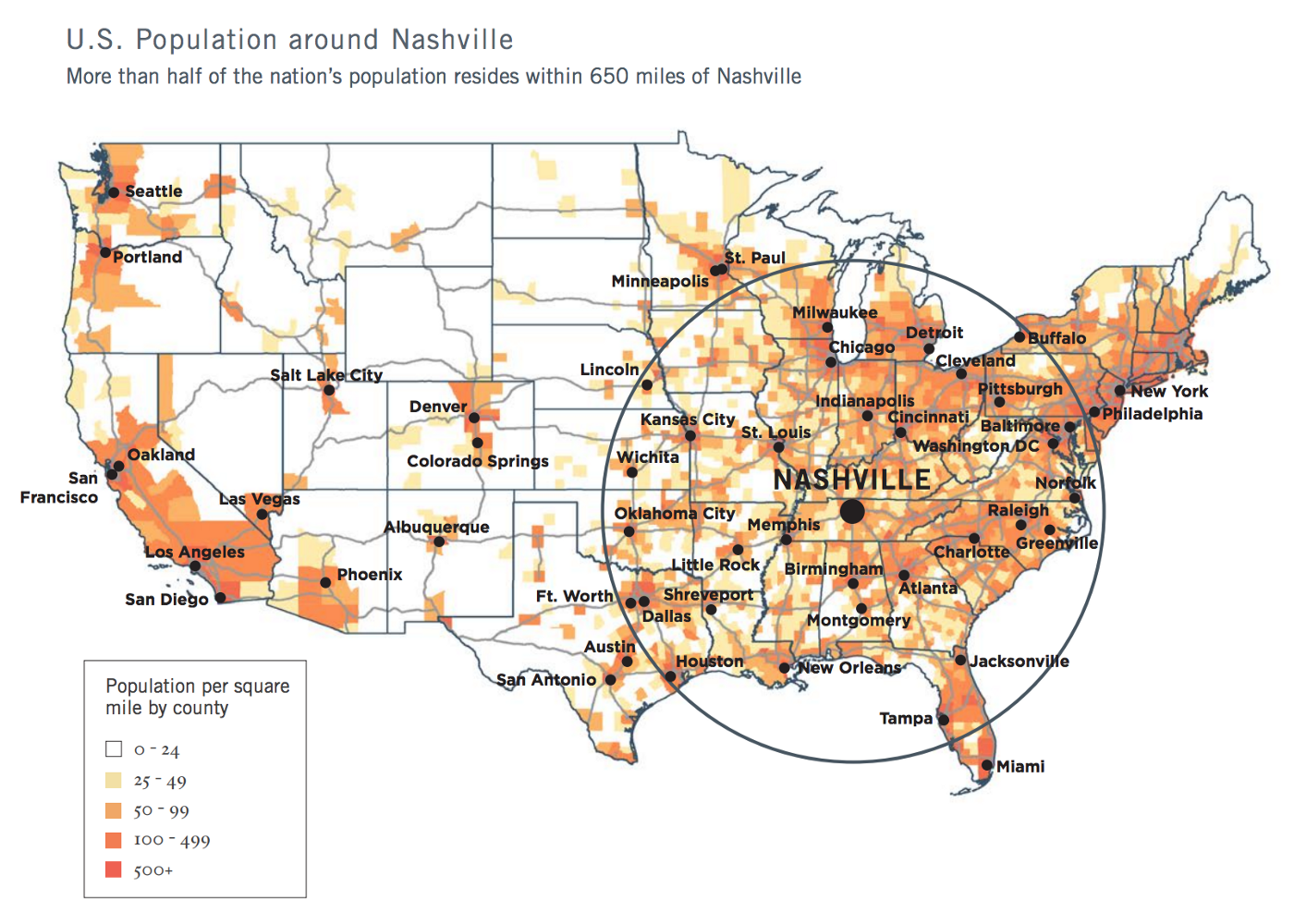

U.S. population around Nashville, TN. Image Credits: Nashville 2018 Regional Economic Development Guide

I wrote about the unfair advantage of Nashville back in 2018 when I announced the launch of Build In SE, a community I co-founded to support founders choosing to build their companies in the Southeast. Nashville is at the center of over half of the United States population within a radius of 650 miles, and within a two-hour flight of 75% of the U.S. market.

Customers come in all shapes and sizes, and founders with boots on the ground in these markets, wearing the same brand of proverbial boots as these customers, carry an unfair advantage. These same founders historically bootstrapped their companies out of need, as access to early-stage, high-risk capital can be scarce and vary widely city by city, state by state, industry by industry.

These same founders still built household name companies in the tech and innovation economy, including the likes of Mailchimp, Calendly, Lynda.com, and GoFundMe (their Series A valued them at $600 million pre-money). All of these companies have another thing in common — they were founded “beyond Silicon Valley.”

Another macrotrend at play is that of the increasing distribution of talent beyond traditional metropolitan strongholds like San Francisco and New York. Entrepreneurs, technologists and operational talent are lifestyle-seeking at a time in history when life feels all the more precious. Moving to cities like Nashville, Austin, Atlanta, Denver, Durham, Miami, et. al. means proximity to aging family members, affordable childcare and outdoor activities.

These simple pleasures were the tradeoffs people made when “pursuing their dreams” in coastal cities, picking up to move in pursuit of money (sometimes better weather). Seemingly overnight, capital abounds in the private markets just as talent becomes increasingly scarce and therefore valuable. The pendulum swung, and capital became the weaker of the two magnets; Wall Street began moving up Manhattan island toward coffee shops and dog parks when talent began to pose the question, “How long do I want my commute to be?” and “How much time do I want to reclaim for my family, and myself?”

2020 was the match to ignite this dry hillside. People trapped inside of cramped quarters with resources left to invest in a new life (or in other cases, left with nothing to lose) packed their bags for a new, up-and-coming metro.

For some, this comes with a newfound sense of community and belonging, as I experienced in 2017 when I moved from my lifelong home of Los Angeles to Nashville. In LA, my local neighborhood hardly knew one another due to the transient nature of the town. In Nashville, I became part of something greater than myself.

One of the big frustrations expressed by founders I know in markets like Nashville, Atlanta, the Research Triangle, Cincinnati and Toronto, is, “I keep hearing there is more capital available, but I’m not seeing it.” They will meet with investors, then be told they are too early, raising too little money, or too much, or not going after a “big enough market.”

Sometimes, one or more of these may be true. However, there are instances where these investor responses may be thinly veiled criticism of the perceived ability of the founders who might not sound, look or behave like Silicon Valley entrepreneurs.

Closing this gap of understanding between pattern-matching VCs of varying skill and startup CEOs across the country will require hard work in the coming decade. A big piece of this will require breaking bread as neighbors, with kids in the same schools, a shared affinity for the local greasy spoon and a mutual trust. This will be step one. Though really, it will require much more alignment and rigor around the very definition of America.

It is up to investors to capture this opportunity in the next decade. In fact, it is our job.

Powered by WPeMatico

Landed, a startup aiming to improve the hiring process for hourly employers and job applicants, is officially launching its mobile app today. It’s also announcing that it has raised $1.4 million in seed funding.

Founder and CEO Vivian Wang said that the app works by asking applicants to fill out a profile with information like work experience and shift availability, as well as recording videos that answer basic common interview questions. It then uses artificial intelligence to analyze those responses across 50 traits such as communication skills and body language, then matches them up with job listings from employers.

Landed has been in beta testing since March of last year — yes, right as COVID-19 was hitting the United States. Wang acknowledged that this was bad news for some of the startup’s potential customers, but she said businesses like grocery stores and fast food restaurants needed the product more than ever.

“That’s why we continuously grew through 2020,” she said.

After all, Landed allowed those businesses to continue hiring without having to conduct large group interviews in person. Even beyond health concerns, she said managers struggle with rapid turnover in these positions (something Wang saw herself during her time on the corporate team at Gap, Inc.) and with a hiring process that’s usually “only a small part of their job.” So Landed saves time and automates a large part of the product.

Landed CEO Vivian Wang. Image Credits: Landed

Meanwhile, Wang said job applicants benefit because they can find jobs more easily and quickly, often within a week of creating a profile. She also argued that Landed can improve on existing diversity and inclusion efforts by allowing managers to see a broader pool of candidates, and because its AI matching isn’t subject to the same unconscious biases that employers might have.

Of course, bias can also be inadvertently built into AI, but when I raised this issue, Wang pointed to Landed’s partnerships with local nonprofits to bring in underrepresented candidates, and she added, “AI can be scary when there are no human checks in place. We partner directly with our employers to ensure the matches that we’re sending them are the right matches, and there are calibration periods.”

Landed is free for job applicants, while it charges a monthly fee to employers, with customers already including Wendy’s, Chick-fil-A and Grocery Outlet franchisees. In fact, Grocery Outlet Ventura owner Eric Sawyer said that by using the app, he’s gone from hiring one person for every 10 interviews to hiring one person for every three interviews.

“My time spent on scheduling and performing interviews has been cut in half by utilizing the Landed app for most of my communications,” he said in a statement.

The new funding was led by Javelin Venture Partners, with participation from Y Combinator, Palm Drive Capital and various angel investors. Wang said this will allow Landed to continue expanding — the service is currently available in seven metro areas (Northern California; Southern California; Virginia Beach/Chesapeake, Virginia; Phoenix/Scottsdale, Arizona; Atlanta, Georgia; Reno, Nevada and Dallas-Ft. Worth, Texas), with a goal of tripling that number by the end of the year.

Wang added that eventually, she wants to provide other services to job applicants, such as loans (at a lower rate than payday lenders) and job training, turning Landed into a “lifestyle stability platform” that combines job stability, financial stability and educational “upskilling” for blue-collar workers.

Powered by WPeMatico

Atlassian has made it clear for some time that it’s all in on the cloud, but now it’s official. The company stopped selling new on-prem server licenses as of yesterday. Perhaps to take away the sting of that move for large organizations, today it announced a new all-inclusive enterprise pricing tier.

Atlassian chief revenue officer Cameron Deatsch says that previously the company had offered a free tier and then standard and premium-level paid tiers. “And now this cloud Enterprise Edition will be our highest tier, and what this will allow is for the most complex deployments, the largest customers who need unlimited scale, the customers that have all the security and regulatory requirements, data residency, you name it, — that is what we’re launching starting [today],” Deatsch told me.

What the enterprise tier delivers is unlimited instances across the Atlassian product line for each enterprise customer. That means a big company with multiple divisions could, for instance, have 20 instances of Jira and Confluence deployed with one for each division and a central management console.

While the company is supporting existing on-prem server customers until 2024, the idea is to now move them to the cloud and this offering should help. One thing we have clearly seen is that the pandemic has accelerated the move to the cloud by companies of every size, and this should encourage the company’s largest customers to make the move.

“The reality is, the demand was there, which was great to see, but we actually had this huge pipeline of our largest customers, basically trying to build their plan over the next couple of years to get to our cloud. The general availability of our Enterprise Edition is going to accelerate that even more,” he said.

It’s a move the company has been working toward for some time, but it really began to take shape when they shifted their operations to AWS and rebuilt the entire stack as a set of microservices beginning in 2016. This was the first step toward being able to handle the increased kinds of workloads an enterprise tier would require.

The company reported earnings at the end of last month with revenue of $501.4 million up 23% YoY with over 11,000 net new subscribers, a record for the company. The new enterprise tier won’t help with new customer volume, but it should help with overall revenue as more customers look for cloud solutions and pricing that meets their needs.

Powered by WPeMatico

For the longest time, Acrobat was Adobe’s flagship desktop app for working with — and especially editing — PDFs. In recent years, the company launched Acrobat on the web, but it was never quite as fully featured as the desktop version, and one capability a lot of users were looking for, editing text and images in PDFs, remained a desktop-only feature. That’s changing. With its latest update to Acrobat on the web, Adobe is bringing exactly this ability to its online service.

“[Acrobat Web] is strategically important to us because we have more and more people working in the browser,” Todd Gerber, Adobe’s VP for Document Cloud, told me. “Their day begins by logging into whether it’s G Suite or Microsoft Office 365. And so we want to be in all the surfaces where people are doing their work.” The team first launched the ability to create and convert PDFs, but as Gerber noted, it took a while to get to the point where being able to edit PDFs in a performant and real-time way was possible. “We could have done it earlier, but it wouldn’t have been up to the standards of being fast, nimble and quality.” He specifically noted that working with fonts was one of the more difficult problems the team faced in bringing this capability online.

He also noted that even though we tend to think of PDF as an Adobe format, it is an open standard and lots of third-party tools can create PDFs. That large ecosystem, with the potential for variations between implementations, also makes it more difficult to offer editing capabilities for Adobe.

With today’s launch, Adobe is also introducing a couple of additional browser-based features: protecting PDFs, splitting them into two and merging multiple PDFs. In addition, after working with Google last year to offer a handful of Acrobat shortcuts using the .new domain, Adobe is now launching a set of new shortcuts like EditPDF.new. The company plans to roll out more of these over the course of the next year.

In total, Adobe says, the company saw about 10 million clicks on its existing shortcuts, which just goes to show how many people try to convert or sign PDFs every day.

As Gerber noted, a lot of potential users don’t necessarily think of Acrobat first. Instead, what they want to do is compress a PDF or convert it. Acrobat Web and the .new domains help the company bring a new audience to the platform, he believes. “It’s unlocking a new audience for us that didn’t initially think of Adobe. They think about PDFs, they think about what they need to do with them,” he said. “So it’s allowing us to expand our customer base by being relevant in the way that they’re looking to discover and ultimately transact. Our journey with Acrobat web actually started with that notion: let’s go after the non-branded searches.”

Adobe, of course, funnels to the Acrobat desktop app all branded searches where users are explicitly looking for Acrobat, but for the more casual user, it brings them to Acrobat Web where they can easily perform whatever action they came for without even signing up for the service.

Powered by WPeMatico

The growth of remote working and managing workforces that are distributed well beyond the confines of a centralized physical office — or even a single country — have put a spotlight on the human resources technology that organizations use to help manage those people. Today, one of the HR startups that’s been seeing a surge of growth is announcing a round of funding to double down on its business.

Oyster, a startup and platform that helps companies through the process of hiring, onboarding and then providing contractors and full-time employees in the area of “knowledge work” with HR services like payroll, benefits and salary management, has closed a Series A round of $20 million.

The company is already working in 100 countries, and CEO and Tony Jamous (who co-founded the company with Jack Mardack) said in an interview that the plan is to expand that list of markets, and also bring in new services, particularly to address the opportunity in emerging markets to hire more people.

Currently, Oyster does not cover candidate sourcing or any of the interviewing and evaluation process: those could be areas where it might build its own tech or partner to provide them as part of its one-stop shop. It has dabbled in virtual job fairs, as a pointer to one potential product that it might explore.

“There are 1.5 billion knowledge workers coming into the workforce in the next 10 years, mostly from emerging economies, while in developed economies there are some 90 million jobs unfilled,” Jamous said. “There are super powers you can gain from being globally distributed, but it poses a major challenge around HR and payroll.”

Emergence Capital, the B2B VC that has backed the likes of Zoom, Salesforce, Bill.com and our former sister site Crunchbase, is leading the funding. The Slack Fund (Slack’s strategic investment vehicle) and London firm Connect Ventures (which has previously backed the company at seed stage) are also participating. The investment will accelerate Oyster’s rapid growth, and support its mission of enabling people to work from anywhere.

Oyster’s valuation is not being disclosed. The startup has raised about $24 million to date.

One of the great ironies of the global health pandemic is that while our worlds have become much smaller — travel and even local activities have been drastically curtailed, and many of us spend day in, day out at home — the employment opportunity and scope of how organizations are expected to operate has become significantly bigger.

Public health-enforced remote working has led to companies de-coupling workers from offices, and that has opened the door to seeking out and working with the best talent, regardless of location.

This predicament may have become more acute in the last year, but it’s been one that has been gradually coming into focus for years, helped by trends in cloud computing and globalization. Jamous said that the idea for Oyster that came to him was something he’s been thinking about for years, but became more apparent when he was still at his previous startup, Nexmo — the cloud communications provider that was acquired by Vonage for $230 million in in 2016.

At Nexmo we wanted to be a great local employer. We were headquartered in two countries but wanted to have people everywhere,” he said. “We spent millions building employment infrastructure to do that, becoming knowledgeable about local laws in France, Korea and more countries.” He realized quickly that this was a highly inefficient way to work. “We weren’t ready for the complexity and diversity of issues that would come up.”

After he moved on from Nexmo and did some angel investing (he backs other distributed work juggernauts like Hopin, among others), he decided that he would try to tackle the workforce challenge as the focus of his next venture.

That was in mid-2019, pre-pandemic. It turned out that the timing was spot on, with every organization looking in the next year at ways to address their own distributed workforce challenges.

The emerging market focus, meanwhile, also has a direct link to Jamous himself: He left his home country of Lebanon to study in France when he was 17, and has essentially lived abroad since then. But as with many people who move from developed into emerging markets, he knew that the base of technical talent in his home country was something that was worth tapping and nurturing to help residents and the countries themselves improve their lots in life; and he thought he could use tech to help there, too.

Related to that wider social mission, Oyster has a pending application to become a B-Corporation.

Jamous is not the only one that has founded an HR company based on his personal experience: Turing’s founders have cited their own backgrounds growing up in India and working with people remotely from there as part of their own impetus for building Turing; and Remote’s founder hails from Europe but built GitLab (where he had been head of product) based on a similar premise of tapping into the talent he knew existed all around the world.

And indeed, Oyster is not alone in tackling this opportunity. The list of HR startups looking to be the ADPs of the world of distributed work include Deel, Remote, Hibob, Papaya Global, Personio, Factorial, Lattice, Turing and Rippling. And these are just some of the HR startups that have raised money in the last year; there are many, many more.

The attraction of Oyster seems to come in the simplicity of how the services are provided — you have options for contractors and full-timers, and full, larger staff deployments in other countries. You have options to add benefits for employees if you choose. And you have some tools to work out how hires fit into your bigger budgets, and also to guide you on remuneration in each local market. Pricing ranges from $29 per person, per month for contractors, to $399 for working with full employees, to other packages for larger deployments.

Oyster works with local partners to provide some aspects of these services, but it has built the technology to make the process seamless for the customer. As with other services, it essentially handles the employment and payroll as a local provider on behalf of its customers, but can do so under contract terms that reconcile both a company’s own policies and those of the local jurisdictions (which can differ widely between each other in areas like vacation time, redundancy terms, maternity leave and more).

“It has a few well-funded competitors, but that’s usually a good signal,” said Jason Green, the Emergence partner who led its investment. “But you want to bet on the horse that will lead the race, and that comes down to execution. Here, we are betting on a team that’s done it before, an entrepreneur experienced in building a company and selling it. Tony’s made money and knows how to build a business. But more than that, he’s mission driven and that will matter in the space, and to employees.”

Powered by WPeMatico

In a creator-economy world, if you’re only as good as your last YouTube video, then your next YouTube video had better be bigger and louder than the last.

Vibely, a new startup co-founded by Asana alumni Teri Yu and Theresa Lee, wants to turn the constant, and often exhausting, beast of content creation on its head. The startup has created a premium, creator-controlled community platform that allows fans to gather and be monetized in new ways, beyond what is possible on YouTube or TikTok.

The core of Vibely, and what the co-founders hope will keep users coming back, is the ability to let any creator make a challenge for their fans to enjoy. For example, a creator whose brand evokes thoughtfulness could ask fans to sketch out their personal growth goals or take action around a new year’s resolution everyday. Or a fitness influencer could motivate fans to work out for a sprint of days.

“Most people in the creator economy are thinking about how to immediately monetize and get that instant gratification of like money here,” Yu said, which is why creators sell merchandise or hop on Cameo. “We’re focusing on long-term strategic communities.” Yu describes her startup’s shift as a mindset change, from a linear relationship between creators and fans to a multi-directional relationship between fans, superfans, new fans and creators.

Image Credits: Vibely

Vibely’s pitch is two-fold. For fans, the platform gives them a chance to chat with other fans from around the world. It also lets fans participate in community challenges and have a place to plan virtual hangouts over shared love for makeup or dance. The startup helps creators simultaneously, by giving them a one-stop shop to announce plans, do call to actions and create an ambassador program. It lets the “creator scale their time and have a multi-directional relationship with the community under or beneath them.”

Notably, Vibely is trying to be different from Patreon or OnlyFans, which is basically paywalled content for fans. Vibely doesn’t need creators to post more content, it just needs them to pop into a premium community and interact with fans in a meaningful way.

The startup is formalizing a sporadic daily occurrence: When a creator posts content, their comment sections in YouTube, Instagram and TikTok light up with fans discussing every detail you can imagine, from a suggestive hair flip to if that background poster has a hidden message. Creators often pop in to respond to a spicy thread or a random compliment, which incentivizes fans to keep swarming the content section.

The startup has spent little on customer acquisition cost and relied heavily on word of mouth. In December, Vibely launched a part-in-person, part-virtual creator house to pair top TikTok creators with their followers, generating some buzz. In 2020, Vibely had more than 600 communities with 392,000 messages sent and 37,000 challenges completed. Creators include Lavendaire, with 1.3 million YouTube subscribers and Rowena Tsai, who has 520,000 subscribers.

Yu says that there is one day where Kim Kardashian might have a community on the platform, but the main “bread and butter” of Vibely is searching for creators who represent a true interest, value or belief system. This can be a book influencer or a religious creator, for example.

“[Creators] are controlling their own destiny,” Yu said. “On Instagram or Facebook, you might create content but the algorithm decides at the end of the day whether or not your audience sees it. With Vibely, they have 100% control since this is their community.” The startup is planning to make money through membership dues and in-app mechanics like social currencies and rewards.

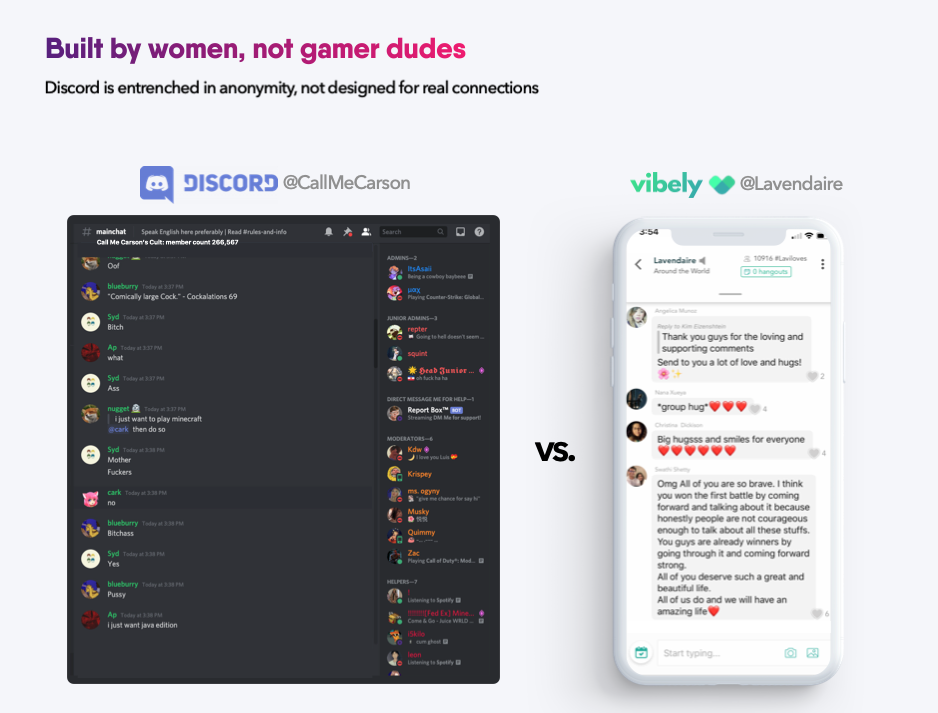

Vibely’s moonshot goal is to be a more positive, and supportive, Discord, a platform used by gamer communities across the world. So far, Yu says that less than .1% of Vibely users have been flagged by other users, although notably would not share total user numbers. There is also an ambassador program that appoints a user to oversee a community, as well as a global community manager on the team.

“The ceiling of where [Discord] can support is really only going to be gamers,” she said. “But creators want to protect their brand right now and make sure people have a positive experience,” so they are looking for another place to set up.

Image Credits: Vibely

While moderation is apparently going well so far, Vibely will most certainly encounter problems as more and more users join its platform. In the world of challenges, craze and hype led by fanatics could potentially become harmful if someone takes it too far. While Vibely aims to be a judgement-free zone for people to connect around the world, scale has a uniquely pessimistic way of forking that from time to time. Some consumer apps have responded to this truth by aggressively hiring on-staff moderators, but that too can become grueling work.

To hit the ground running, Vibely announced today that it has raised $2 million in seed financing from backers including Steve Chen, the co-founder of YouTube; Justin Rosenstein, the co-founder of Asana and co-creator of Netflix’s “Social Dilemma” documentary; Scott Heiferman, the co-founder of Meetup; Turner Novak, formerly an investor at Gelt, and more.

Powered by WPeMatico

Last year I penned a post positing that Salesforce’s propensity to purchase mature enterprise companies not only provided new technology, but was also helping to produce a profusion of executive talent. As though to prove my point, the company announced today that it was promoting former Vlocity CEO David Schmaier to president and chief product officer.

Schmaier came to the organization last year when Salesforce acquired his company for $1.33 billion. It seemed like a good match, given that Vlocity sold Salesforce solutions designed for certain niches like financial services, health, energy and utilities and government and nonprofits.

As a result, Schmaier knew the product set and the company well. Last June, he was named CEO of the Salesforce Industries division, which was created after the Vlocity acquisition. The connection was clear to Schmaier as he told me at the time of his promotion last year:

“I’ve been involved in various mergers and acquisitions over my 30-year career, and this is the most unique one I’ve ever seen because the products are already 100% integrated because we built our six vertical applications on top of the Salesforce platform. So they’re already 100% Salesforce, which is really kind of amazing. So that’s going to make this that much simpler,” he said.

Brent Leary, founder and principal analyst at CRM Essentials, says that Schmaier’s history in building Vlocity makes this promotion pretty easy given the direction of the company, as well as the industry. “Over the last several years we’ve seen just how important developing industry-specific solutions have become to the major players in the space, and Schmaier’s promotion reaffirms this while illustrating how important creating verticals is to their platform [and] to the future of Salesforce,” he told me.

In a Q&A on the Salesforce website announcing the promotion, Schmaier talked about the challenges companies faced in the last year. “There’s no question 2020 was a challenging year. We are operating in this all-digital, work from anywhere world and things won’t go back to where they were, nor should they. One of the silver linings has been seeing what companies can do when there is no alternative and the imperative is to connect with their customers in entirely new ways,”

In his new position it will be Schmaier’s job to figure out how to help them do that.

It’s worth noting that there has been some turnover in the C Suite recently at Salesforce. Just today the company also announced that long-time CFO Mark Hawkins was retiring. He will be replaced by Amy Weaver, who was formerly the company’s chief legal officer. Meanwhile, last week the company hired former Hearsay Social co-founder and CEO Clara Shih to run Salesforce Service Cloud.

Powered by WPeMatico

Soon all tech news will be fintech news, all fintech news will be trading platform news and all trading platform news will concern the business mechanics of such services.

So, after looking into Robinhood’s fourth-quarter payment for order flow (PFOF) revenues this morning, we’re back with a related story. This time, however, we’re talking about Public.

Public, like Robinhood, is a zero-cost trading service. Its founders have worked to build a community-first platform, including offering ways to let groups chat about their investments.

And like Robinhood, Public has seen its growth skyrocket in recent days. Company representatives told TechCrunch today it was seeing “steady ~30%” month-over-month growth until Thursday, when “new user signups went up 20x.”

Both share strong backing from investors: Robinhood raised billions in new capital this week to ensure it has enough cash to meet clearinghouse deposit requirements. It managed to do so in part because its Q4 2020 numbers show that its PFOF business is ticking along nicely.

Public, flush with a recent $65 million Series C, took a different tack this morning and announced it would “stop participating in the practice of Payment for Order Flow.”

To which we say … all right.

On one level, this is neat. Public is not going to sell its order flow to market makers for fees. That’s good for users, but how will it make up the lost revenue? Tips, which will prove an interesting experiment in monetization.

TechCrunch asked the company if it believes tips will compensate for PFOF revenue, to which founders Leif Abraham and Jannick Malling replied via email that they were “optimistic that the difference will be offset by the optional tipping feature.”

However, dropping payment for order flow is only so brave a move from Public. After all, Public was not making Robinhood-level amounts of fetti from its PFOF business. Indeed, as we wrote when Public raised its Series C:

Before chatting with Public, I dug into its trading partner Apex’s filings to learn about its payment for order flow results from its recent filings. The resulting sums are somewhat modest for Apex’s collected clients. This means that Public’s revenue metrics, a portion of the aggregate sums, are even more unassuming.

Powered by WPeMatico

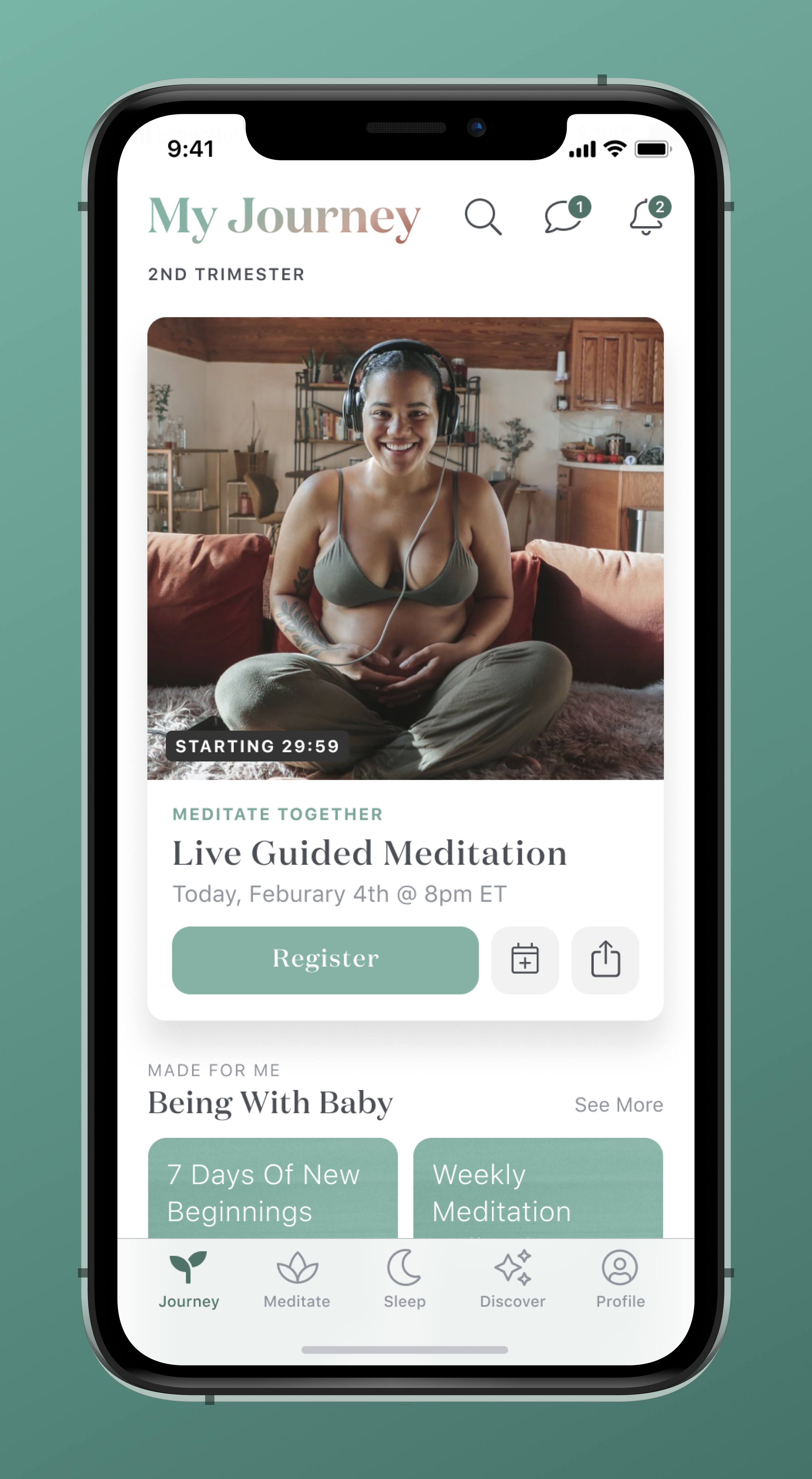

Nathalie Walton almost didn’t become a mother. Her risky pregnancy caused her placenta to burst during childbirth, almost killing her and her son last year. Walton, who feels lucky to have survived, says the haunting experience made her an example of a reality she had long known: To be a pregnant Black woman is to be at risk, regardless of economic background.

The stress of her pregnancy led Walton to download Expectful, a meditation and sleep app for new mothers. She recalls stabilizing, emotionally and physically, within a week, bringing an otherwise “soft landing” to a volatile pregnancy.

Weeks after delivering her son, Everett, Walton just so happened to hear of an advisory role opening at Expectful. Even though she was mid-maternity leave from her managerial role at Airbnb, she jumped at the opportunity.

“I definitely had a full-time job, I had a newborn baby,” Walton said. But, she says, it was an opportunity to be entrepreneurial in a sector she cared about. Even if it was just for a few months.

And now, Walton is the chief executive of the company. The business is pivoting its product strategy to grow beyond recorded meditations. Walton helped it raise its first millions in venture capital, making her one of the few dozen Black female founders to do so. New financing and the boom of the mental health focus amid the coronavirus pandemic puts Expectful in a coveted spot. And it puts Walton, who is at the helm of a company for the first time, in a pressure-cooker spotlight.

Even in the world of startups, going from user to chief executive in less than a year is a remarkable feat. But it’s not one that she rushed.

Walton graduated from Georgetown and immediately joined the New York banking world. After a few years as an analyst at JP Morgan, though, she became unsatisfied with the work.

“I think I had a quarter-life crisis,” Walton said. Searching for new opportunities, she ended up at a prospective students day at Stanford University in what would become a pivotal moment in her life.

“For the first time, I met entrepreneurs and saw an actual concept that you can pursue a career you like, be successful and make a difference in the world,” she said. Walton eventually applied, and got accepted, to Stanford Graduate School of Business (GSB), a prestigious program that produces founders and top executives. It was then that she realized she wanted to be a chief executive one day.

“I admired them, but I just didn’t see the pathway for me to get there,” she said, of the entrepreneurs she met, who were then largely white and male. “I didn’t have the confidence.”

So, she set that hope aside and pursued intrapreneurship, which would let her join a stable organization and act as a mini-founder within it. Employees in this role are tasked with building a startup within a startup, whether that is rooting an innovative idea or leading an experiential team. Corporations have long embraced this idea to bring momentum to otherwise red-tapey processes.

Walton joined eBay and soon rose to work as the head of business operations and development. Her work helped the company break into 3D printing.

Over the years, this has been the defining characteristic of Walton: join an organization, build a scrappy idea from scratch, and then do it all over again. She has held roles in Airbnb and Google that all required her to have the agility of a founder convincing people on a moonshot vision, and the rigor of a manager who can get a deal done.

She had the same vision heading into an advisory role at Expectful. But when Walton landed a key Expectful partnership with Johnson & Johnson, then-CEO and founder Mark Krassner had an idea.

Before starting Expectful, Krassner experienced the benefits of meditation firsthand. He also saw his mother face depression, which made him realize how meditation could have a positive impact on others. After seeing research that showed how meditation could positively impact a pregnancy, he began thinking of a solution in this cross-section. He eventually started a course on Teachable, a startup that lets anyone create and monetize an online class, with 15 moms and a guided meditation.

Over time, the idea stuck. Krassner eventually turned his course into a 12-person startup. Under his leadership, Expectful grew to profitability and over 13,000 paid users. Its conversion rate from free to paid users was five times higher than industry standards, the company claims.

That said, from the moment Mark Krassner started Expectful, he knew he was an unlikely founder. He doesn’t have any children, so leading a meditation and sleep app for new mothers comes with its own hurdles.

“As a male founder with no kids, it was on my mind from day No. 1,” Krassner said. He eventually wanted to put a female at the head of the company, he says. Walton was the obvious choice.

Walton returned to Airbnb after her maternity leave right as Airbnb had aggressive COVID-19 layoffs. While her job was saved, her team disappeared as part of the cuts. She started looking for jobs, and received lucrative offers from Facebook, Apple, Google and Amazon. When she told Krassner she was leaning toward a lead product manager position at Amazon, he replied with an offer to take over Expectful’s entire business.

“I think it caught her off guard,” Krassner said, who is still a board member at the company. “Usually you don’t think a CEO is looking for [a new CEO] unless things are going to hell in a handbasket.”

Expectful began as a guided meditation library, which will continue to be its core. But now, Walton wants to take advantage of that momentum and evolve the company into a “go-to wellness resource for hopeful, expecting and new parents.”

The language suggests that the startup is evolving in how it markets itself. Right now, the site has a number of references to “motherhood” and women. But Walton says Expectful defines a mother by anyone who identifies themselves as one. While the startup primarily has content geared toward the gestational parent, or the one who gives birth to the child, Walton says they have a “a partner’s library for non-gestational parents that identify as non-gestational mothers, fathers, or however they choose to identify.”

Walton plans to pivot the startup in three phases: content, marketplace and community.

For content, Expectful wants to organize pregnancy-related information. Currently, a lot of information or advice around pregnancy lives in books or in-person classes. But the learning experience, which Walton says is similar to middle school-style lectures, doesn’t feel built for this century.

The next step in her plan is digitizing the service providers that help women through pregnancy. In simpler words, replace the disorganized recommendations in Facebook groups for parents.

“When I went to ask my OB-GYN for recommendations for a doula, she gave me a sheet of paper with the names of 10 doulas,” she said. “You have to text the doula, ask them questions and if they want to meet up — it all feels yucky.” Expectful wants to put all that information in one platform so moms can access tips and recommendations from the ease of their homes.

The end-product here would be a peer-reviewed platform that can help a mom find everything from a therapist to a live-in nanny, with reviews built-in.

Finally, Walton wants to invest in the community. Expectful recently launched Mother Circles, which connects postpartum mothers into support cohorts led by a doula facilitator. The circles include six weekly video calls, a group chat and 500 hours of on-demand doula support.

Image Credits: Expectful

Part of Walton’s focus through all of these priorities is to invest in Black maternal health outcomes. Her own experience, she says, showed her how even a “Stanford-educated wellness junkie” such as herself can be at a high-risk for pregnancy because of her skin color.

It’s a lofty goal, even with the promising growth and strong library of guided meditations. The competition is steep. One of Expectful’s closest competitors is Peanut, a social network for moms used by over 1.2 million people. Mahmee, a digital support network for postpartum mothers, has raised $3 million and views itself as complementary to Expectful. Headspace has launched its own motherhood meditation series, but it is not as comprehensive as Expectful’s.

“I think we’re able to connect with women in a way that some of these other companies aren’t,” Walton said. “People are paying for the service, so they clearly need it.”

While Walton declined to share new user metrics, she said that the company’s revenue has grown 100% since March 2020.

Long-term, Expectful wants to mimic Peloton’s playbook in terms of getting premium content and community to the right audience. Still, growing from a startup to a venture business requires more than just ambition and market fit. It requires the ability to exponentially grow and keep growing.

A handful of investors believe that Walton’s Expectful can do it. Expectful raised $3 million in a seed financing round led by Harlem Capital. Indicator Ventures, Sequoia Scout Fund, Joyance Partners, Break Trail Ventures, Chinagona Ventures, Powerhouse Capital, AVG Basecamp Fund and Babylist also participated. Angel investors included Ellen Pao, Mike Smith and Ashley Mayer. The round also included $1.2 million in convertible SAFE notes, making the financing round a total of $4.2 million.

“Historically when I look at what black women raise fundraising, I feel fortunate that I’ve been able to raise this round,” Walton said.

Harlem Capital founding partner Henri Pierre-Jacques said that “obviously, given our focus we weren’t going to invest in a white male.” Walton’s “founder-market fit” is what made the firm invest, even with the hairy dynamic of an exiting CEO.

Mayer, head of communications at Glossier, was the one who introduced Walton to the woman who told her about the advisory role of Expectful. She says that Nathalie’s “path to entrepreneurship feels inevitable.

“It was always just a question of finding the space where her passions collided,” Mayer said.

As a new mother and new founder, Walton has had a busy balancing act of a year.

“I’m working more now than I have really in the last decade,” she said. “But I’ve never been more fulfilled because, as someone who went through this, and I’m still going through this, I feel so personally the level of pain that so many women suffer through.”

Powered by WPeMatico

Every sport has its practice drills and exercises to help players hone skills between games. Why would esports be any different?

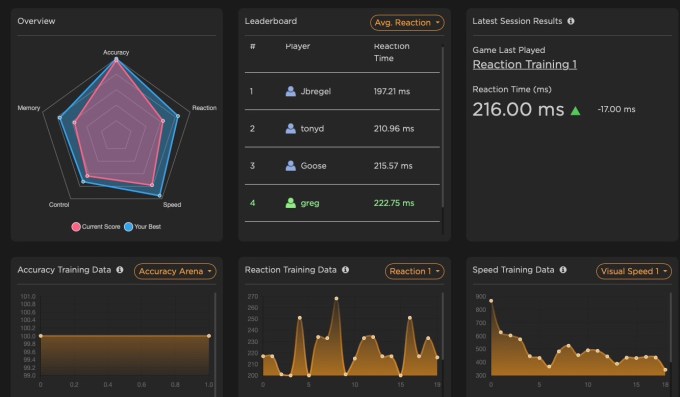

Gwoop, a startup out of Minnesota, wants to be the place where gamers go to train between matches. They’re building up a collection of free browser-based training tools meant to help you measure and improve vital stats like reaction time, mouse control, and aim, and see how your stats compare to the best.

Some of the training games currently up and running:

Image Credits: Gwoop

All of the tools are linked back to an analytics dashboard, allowing you to gauge your performance metrics over time. Each skill gets its own leaderboard so you can see, for example, how your average reaction time compares to others worldwide and amongst your friends.

Even in its 3D exercises, Gwoop’s graphics are pretty simple — and that’s intentional. They want it to work for as many players as possible. They’ve got no reason to try to look like a AAA title; the more graphically intense a game is, the more powerful your computer would have to be to run it smoothly. Co-founder Gavin Lee tells me that their goal is to keep it so that “all you need is a computer and the internet. It doesn’t matter if your device is 10 years old.” Even its 2D exercises have switches you can flip to further simplify the graphics and improve performance.

It’s the same reason they’ve built everything to work in the browser: not requiring any downloads means more people can train, with the added benefit for the Gwoop team of not having to worry about maintaining separate Mac/PC clients.

While the existing exercises might seem focused around improving first-person shooter skills, Lee tells me that they’re aiming to be “genre-agnostic” and are planning expansions tailored to other kinds of games. He mentions a “MOBA Arena” in the works meant to help polish skills required for games like League of Legends or DOTA, and another exercise in progress that’s “very Rocket League-centric.” Their training tools seem mostly focused on keyboard/mouse users right now, but they’re working on more functionality for players who prefer controllers.

Image Credits: Gwoop

Gwoop is entirely free to players — so how will they make money? Lee tells me they’ve got two different strategies there: They’ll sell additional advanced analytics tools to teams, and, once they’ve got enough players clicking around, hopefully be able to serve as a platform for esports recruiters. Lee says players should be able to opt-in to having their data shared with potential sponsors and esports teams, with Gwoop getting paid to connect the dots. “All these division one schools have these platforms where you can upload football films and get recruited,” says Lee “we want to become that platform [for esports].”

Why the name “Gwoop”? Is it a bit of super cool gaming lingo, or some sort of acronym? Nope! It was just a quick, memorable domain Lee had been holding onto for decades. “I wish I had a better story for you,” he says, “but I bought the domain in 2002 just because I wanted a five-letter domain that you could pronounce and was available.” It’s okay, Gavin: Most people don’t care why Google is called Google, after all.

The team’s timing is pretty good here. With most people being stuck at home, more people are getting into gaming than ever before. Battle Royale games like Fortnite, PUBG and Apex Legends are blowing up … but it’s hard to get better in a game where you spend the first 10 minutes looting only to get shredded in 10 seconds when a skilled team rotates through. While many titles have dedicated training areas or firing ranges to practice in, they’re usually meant more for quick pre-game warmups and don’t do things like help you track metrics and improvements over time.

Image Credits: Gwoop

The Minneapolis-based team is currently comprised of its three co-founders. It’s self-funded to date, but I’m told a seed round is underway.

Gwoop is currently in semi-closed beta and generally requires an invite to signup, but Lee tells me that the code #TC2021# should let our readers past the signup gate.

Powered by WPeMatico